English

English Français

Français 日本語

日本語 中文

中文Kamoa mine projected to have the highest grade among the world’s

largest copper mines and also to be one of the world’s

lowest-cost copper producers

Estimated pre-tax NPV of US$4.3 billion and an 18.5% IRR

LUBUMBASHI, DEMOCRATIC REPUBLIC OF CONGO – Robert Friedland, founder and Executive Chairman of Ivanhoe Mines (TSX: IVN), and Lars-Eric Johansson, Chief Executive Officer, today welcomed the positive findings of an independent, Preliminary Economic Assessment of the company’s major Kamoa copper discovery near the mining centre of Kolwezi in the Democratic Republic of Congo’s southern province of Katanga.

“The assessment confirms that Kamoa truly is in a class by itself in terms of the world’s known, undeveloped copper deposits,” said Mr. Friedland.

“Kamoa has the rare combination of a very high copper grade and very large tonnage, qualities that position Kamoa to become a substantial copper producer with one of the lowest cash costs anywhere in the world. This thorough, independent assessment gives us added confidence as we proceed with the planning of our next steps to advance Kamoa’s development into a world-class copper mine.”

Highlights of the Preliminary Economic Assessment (PEA):

- A large mine and smelter would be developed using a two-phased approach.

- A smaller-scale start-up would establish an operating platform to support expansion.

- Early cash flows would be generated from the sale of high-grade copper concentrate.

- Low pre-production capital requirement of approximately US$1.4 billion.

- Steady-state production target of 300,000 tonnes per year of blister copper, which would establish Kamoa as one of the world’s largest copper mines, with the highest grade.

- Cash costs of US$1.18 per pound of copper would rank Kamoa near the bottom of the global cash-cost curve.

- Pre-tax Net Present Value, at an 8% discount rate, of US$4.3 billion.

- After-tax Net Present Value, at an 8% discount rate, of US$2.5 billion.

- Pre-tax internal rate of return of 18.5%; after-tax IRR of 15.2%.

The PEA, which conforms with the requirements of Canada’s National Instrument 43-101, was prepared by AMC Consultants, AMEC E&C Services (AMEC), SRK Consulting, Stantec Consulting International, Hatch and Golder Associates Africa. The full technical report will be filed on SEDAR at www.sedar.com and Ivanhoe Mines’ website atwww.ivanhoemines.com within 45 days of the issuance of this news release.

Two-phased approach to the development of a large mine and smelter

The PEA reflects a two-phased approach to development of the Kamoa Project. The first phase of mining would target high-grade copper mineralization from shallow, underground resources to yield a high-value concentrate. The second phase would entail a major expansion of the mine and mill and construction of a smelter to produce blister copper.

The PEA contemplates the establishment of a conventional copper mine and concentrator complex at Kamoa with an initial mining rate and concentrator capacity of three million tonnes per year. Initial mill feed would come from the Kansoko Sud mineralized zone and lead into the Centrale area of Kamoa’s mineralized zones.

The initial mining rate and concentrate feed capacity of three million tonnes per year would be followed in Year 5 by an additional expansion of eight million tonnes per year in concentrator capacity and the construction of an on-site smelter with a capacity to produce 300,000 tonnes per year of blister copper. In addition, an estimated 1,600 tonnes of sulphuric acid per day would be produced as a by-product in the copper smelting process.The PEA contemplates that the sulphuric acid produced at Kamoa would be sold to copper-oxide mining operations on the Central African Copperbelt that currently purchase acid from Zambia or from overseas.

The production scenario schedules 326 million tonnes to be mined and milled at an average copper grade of 3.0% copper over a 30-year mine life, producing 7.8 million tonnes of payable blister copper (plus 0.5 million tonnes of payable copper in concentrate, in the initial concentrate phase) over the life of the project.

The PEA is preliminary in nature and includes an economic analysis that is based, in part, on Inferred Mineral Resources. Inferred Mineral Resources are considered too speculative geologically to have the economic considerations applied to them that would allow them to be categorized as Mineral Reserves, and there is no certainty that the results will be realized. Mineral Resources do not have demonstrated economic viability and are not Mineral Reserves.

Positive preliminary economic analysis demonstrates Kamoa’s exceptional nature

The preliminary economic analysis is based on a long-term price assumption of US$3.00 per pound for copper and a sales price for sulphuric acid of US$250 per tonne. The economic analysis returns an after-tax Net Present Value (NPV), at an 8% discount rate, of US$2.55 billion. It has an after-tax internal rate of return (IRR) of 15.2% and a payback period of 8.4 years. The life-of-mine average total cash cost, after credits, is US$1.18 per pound of copper.

Table 1: Summary of financial results.

| Before | After | ||

| Taxation | Taxation | ||

| Net Present Value (US$ billion) | Undiscounted | 25.57 | 17.70 |

| 4.0% | 10.37 | 6.85 | |

| 6.0% | 6.68 | 4.23 | |

| 8.0% | 4.29 | 2.55 | |

| 10.0% | 2.70 | 1.44 | |

| 12.0% | 1.64 | 0.71 | |

| IRR | – | 18.5% | 15.2% |

| Project Payback (years) | – | 7.64 | 8.43 |

Table 2: Mining and processing production statistics.

| Total LOM | Conc. Phase Average* | Blister Phase Average* | LOM Average | |

| Total Plant Feed Mined (‘000 t) | 326,064 | 2,417 | 12,183 | 10,869 |

| Quantity Plant Feed Treated (‘000 t) | 326,064 | 3,000 | 12,243 | 10,869 |

| Copper Feed Grade (%) | 3.00 | 4.00 | 2.94 | – |

| Copper Recovery (%) | 85.91 | 85.87 | 85.91 | – |

| Concentrate Produced (‘000 t) | 21,802 | 258 | 805 | 727 |

| Copper Concentrate Grade (%) | 39.00 | 40.40 | 38.91 | – |

| Contained Metal in Concentrate | ||||

| Copper (‘000t) | 8,502 | 104 | 313 | 283 |

| Copper (Mlb) | 18,744 | 230 | 691 | 625 |

| Payable Metal | ||||

| Copper (‘000t) | 8,312 | 103 | 306 | 277 |

| Copper (Mlb) | 18,325 | 227 | 675 | 611 |

* Excludes Year 5 (2022), which is a transition year between concentrate and blister production. Mining averages on Conc. Phase includes Years -2 and -1.

Table 3: Unit operating costs.

| US$/lb Payable Copper | |||

| LOM Average | Conc. Phase* | Blister Phase* | |

| Mine Site Cash Cost | 1.05 | 0.85 | 1.07 |

| Realization Cost | 0.33 | 0.91 | 0.29 |

| Total Cash Costs Before Credits | 1.38 | 1.76 | 1.36 |

| Acid Credits | 0.20 | – | 0.21 |

| Total Cash Costs After Credits | 1.18 | 1.76 | 1.15 |

* Concentrate and blister averages exclude Year 5 (2022), which is a transition year between concentrate and blister.

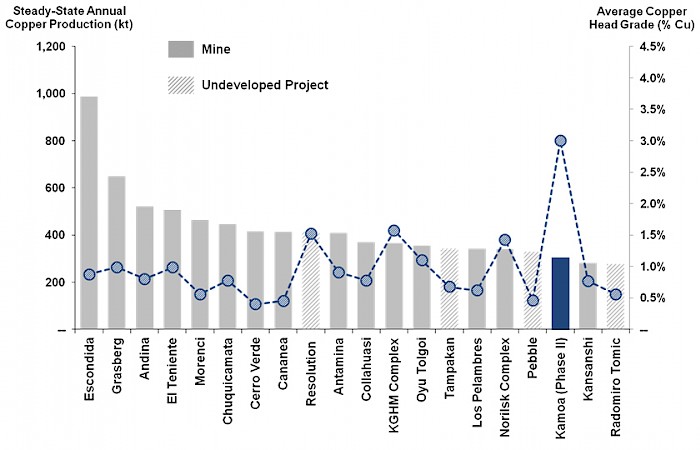

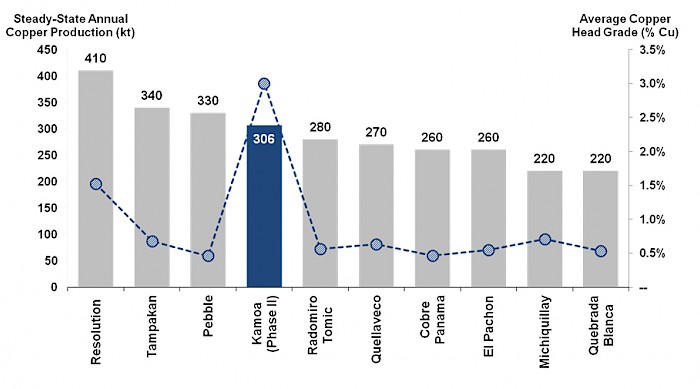

Steady-state production from Year 6 onward of 306,000 tonnes per year of blister copper would establish the Kamoa Project as one of the world’s largest copper mines. Kamoa also would have the highest average grade among the 20 largest copper mines currently in production or expected to be in production, according to data from Wood Mackenzie, an international industry research and consulting group.

Figure 1: Annual copper production for top 20 mines and undeveloped projects globally.

Source: Wood Mackenzie

Figure 2: Annual copper production for all undeveloped projects globally.

Source: Wood Mackenzie

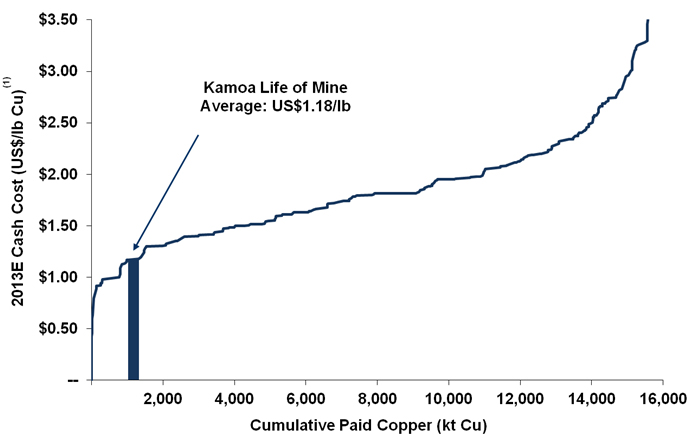

Average cash costs of US$1.18 per pound of copper (after sulphuric acid credit), over the life of the mine, rank the Kamoa Project near the bottom of the 2013 cash-cost curve for copper mines globally.

Figure 3: 2013E copper cash costs.

(1) Represents C1 cash costs that reflect the direct cash costs of producing paid metal incorporating mining, processing and offsite realization costs, having made appropriate allowance for the co-product revenue streams.

Source: Wood Mackenzie

The estimated capital costs for the Kamoa Project are detailed in Table 4, below.

Table 4: Capital investment summary.

| US$M | Concentrate Phase | Blister Phase | Sustaining | Total |

| Mining | ||||

| Underground Mining | 259 | 1,125 | 1,864 | 3,248 |

| Capitalized Pre-Production | 41 | – | – | 41 |

| Subtotal | 301 | 1,125 | 1,864 | 3,290 |

| Power & Smelter | ||||

| Smelter | – | 539 | 297 | 836 |

| Power | 141 | 100 | – | 241 |

| Subtotal | 141 | 639 | 297 | 1,077 |

| Concentrate & Tailings | ||||

| Concentrator | 214 | 312 | 207 | 734 |

| Subtotal | 214 | 312 | 207 | 734 |

| Infrastructure | ||||

| Infrastructure | 81 | 133 | 61 | 274 |

| TSF | 73 | 181 | – | 254 |

| Accommodations | 75 | 10 | 25 | 111 |

| Rolling Stock & Spur | – | 46 | – | 46 |

| Subtotal | 229 | 370 | 86 | 685 |

| Indirects | ||||

| EPCM | 79 | 220 | – | 299 |

| Temporary Facilities | 43 | 78 | – | 121 |

| Subtotal | 122 | 298 | – | 420 |

| Owners Cost (incl. Drilling & Studies) | ||||

| Owners Cost | 103 | 67 | – | 171 |

| Closure | – | – | 166 | 166 |

| Subtotal | 103 | 67 | 166 | 337 |

| Capital Expenditure Before Contingency | 1,110 | 2,812 | 2,621 | 6,543 |

| Contingency | 292 | 717 | – | 1,009 |

| Capital Expenditure After Contingency | 1,402 | 3,529 | 2,621 | 7,552 |

Kamoa discovery forms an extension of the Central African Copperbelt

Ivanhoe Mines’ Kamoa copper project, located in the Democratic Republic of Congo’s (DRC) Province of Katanga, is a newly discovered, very large, stratiform copper deposit with adjacent prospective exploration areas within the Central African Copperbelt, approximately 25 kilometres west of the town of Kolwezi and about 270 kilometres west of the provincial capital of Lubumbashi.

Ivanhoe holds its 95% interest in the Kamoa Project through a subsidiary company, African Minerals Barbados Limited SPRL (AMBL). A 5%, non-dilutable interest in AMBL was transferred to the DRC government on September 11, 2012, for no consideration, pursuant to the DRC Mining Code.

The company also has offered to sell an additional 15% interest to the DRC on commercial terms to be negotiated.

Access to the Kamoa Project from Kolwezi is via unsealed roads. The road network throughout the project area has been upgraded by Ivanhoe to provide reliable drill and logistical access. A portion of the 1,500-kilometre-long railway line and electric power line from Lubumbashi to the Angolan town of Lobito passes approximately 10 kilometres to the north of the project area.

Kamoa was discovered by Ivanhoe in 2008, west of the known limit of the Central African Copperbelt in the DRC. The deposit lies under cover and does not outcrop. The copper mineralization identified at Kamoa is typical of sediment-hosted stratiform copper deposits and is similar to the Polish Kupferschiefer and Zambian Ore Shale deposits. The Kamoa discovery occurs within a regional, northeast-southwest-trending structural corridor that has been traced for approximately 35 kilometres. Copper mineralization at Kamoa has been defined over an area of 20 kilometres by 15 kilometres. The dip of the mineralized body ranges from 0° to 10° near-surface above the Kamoa dome, to 15° to 20° on the flanks of the dome.

In August 2012, the DRC approved Ivanhoe’s application to convert three exploration permits at Kamoa to exploitation permits (mining licences). The Kamoa Mining Licences, covering a total of 400 square kilometres, allow the company to develop and exploit copper and other minerals for a renewable, 30-year term.

A regional exploration program is ongoing, with drilling planned at prospective targets on the more than 9,000 square kilometres of exploration tenements held by Ivanhoe in a variety of geological settings within Katanga Province.

Estimating Kamoa’s Mineral Resources

Resources were classified using a nominal, 400-metre drillhole spacing for classification of Indicated and a nominal, 800-metre spacing for Inferred.

AMEC used a 1% copper cut-off grade as a base case to declare Mineral Resources. This choice of cut-off is based on many years of experience on the Zambian Copperbelt at mines with similar mineralization, such as Konkola, Nchanga, Nkana and Mufulira, where the 1% cut-off is a natural cut-off. The 1% copper cut-off also is a “natural” cut-off for the Kamoa deposit, with most single mineralized zone (SMZ) intercepts (selected using the criteria of a minimum copper grade of 1% copper and a minimum downhole length of three metres) grading a few tenths of a percent copper above and below the composite and well over 1% copper within the SMZ composite. To test the 1% cut-off grade and various sensitivity cases for the purposes of assessing reasonable prospects of economic extraction, AMEC performed a conceptual analysis based on the metallurgical recovery algorithms, operating costs and economic parameters.

The Mineral Resources have been defined taking into account the 2010 CIM Definition Standards for Mineral Resources and Mineral Reserves. Dr. Harry Parker, SME Registered Member, and Gordon Seibel, SME Registered Member, both employees of AMEC, are the Qualified Persons for the Mineral Resource estimates.

Mineral Resources are stated in terms of total copper (Cu). Mineral Resources are reported at a base-case, total copper cut-off grade of 1% copper and a minimum vertical thickness of three metres, and are summarized in Table 5.

Table 5: Indicated and Inferred Mineral Resources, Domain 1.

| Category | Tonnage (Mt) |

Area (km2) |

Cu (%) |

True Thickness (m) | Contained Copper (kt) |

Contained Copper (billion lbs) |

| Indicated | 739 | 50.5 | 2.67 | 5.20 | 19,700 | 43.5 |

| Inferred | 227 | 20.5 | 1.96 | 3.84 | 4,460 | 9.8 |

Notes:

- Domain 1 at 1% Cu cut-off grade.

- Mineral Resources have an effective date of 10 December 2012. Harry M. Parker and Gordon Seibel, both SME Registered Members, are the Qualified Persons responsible for the Mineral Resource estimates. The Mineral Resource estimate was prepared by Mr. Seibel.

- Mineral Resources are reported using a total copper (Cu) cut-off grade of 1% Cu and a minimum assumed thickness of 3 metres. A 1% Cu cut-off grade is typical of analogue deposits in Zambia. There are reasonable prospects for economic extraction under assumptions of a copper price of US$3.30/lb; sulphuric acid credits of US$300/t of acid produced; employment of underground mechanized room-and-pillar mining methods; and that copper concentrates will be produced and smelted.

- Reported Mineral Resources contain no allowances for hanging wall or footwall contact boundary loss and dilution. No mining recovery has been applied.

- The Mineral Resources include the mineralization above a 1% total copper cut-off that is potentially amenable to open-pit mining.

- Tonnage and grade measurements are in metric units. Contained copper tonnes are reported using metric units; contained copper pounds use imperial units.

- True thickness ranges from 2.4 metres to 17.6 metres for Indicated Mineral Resources and 2.8 metres to 8.4 metres for Inferred Mineral Resources.

- Depth of mineralization below the surface ranges from 10 metres to 1,320 metres for Indicated Mineral Resources and 20 metres to 1,560 metres for Inferred Mineral Resources. Indicated Mineral Resources are supported by drilling at a =400-metre spacing; Inferred Mineral Resources are supported by drilling at 400-metre to 800-metre spacing.

- Tonnages are rounded to the nearest million tonnes; grades are rounded to two decimal places.

- Rounding as required by reporting guidelines may result in apparent summation differences between tonnes, grade and contained metal content.

- Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

Additional tonnage estimated in exploration target

The area inside the model perimeter surrounding the Indicated and Inferred Mineral Resources is considered an exploration target. The ranges of the exploration target tonnages and grades are summarized in Table 6.

Tonnage and grade ranges were estimated using an inverse distance to the fifth power for Domain 2 and applying a ±20% variance to the resulting tonnage and grade estimate.

AMEC cautions that the potential quantity and grade of exploration targets are conceptual in nature and that it is uncertain if additional drilling will result in the exploration targets being delineated as a Mineral Resource.

Table 6: Tonnage and grade ranges for Exploration Targets.

| Target | Low-range Tonnage (Mt) | High-range Tonnage (Mt) | Low-range Grade (% Cu) | High-range Grade (% Cu) |

| Total | 520 | 790 | 1.6 | 2.5 |

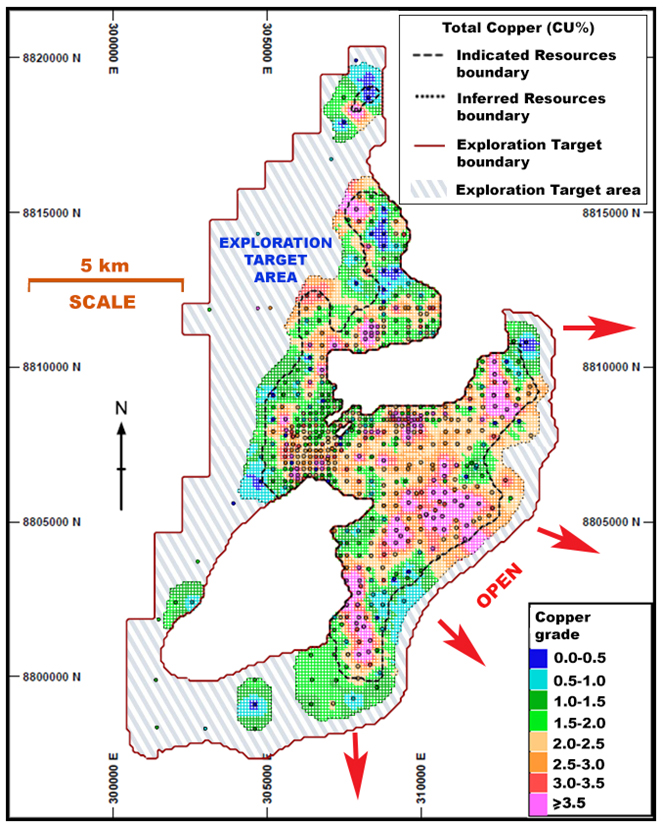

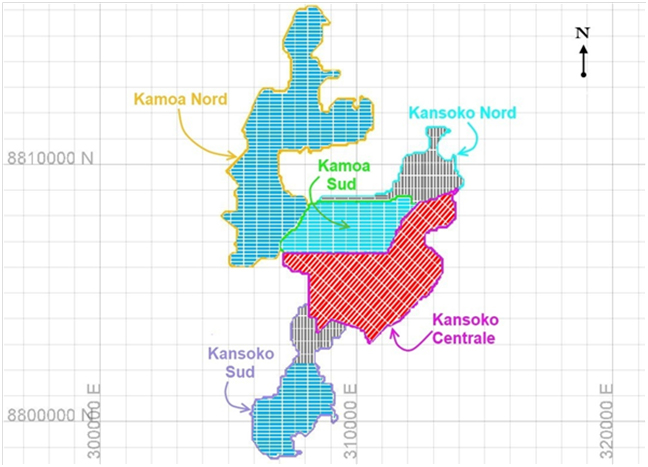

Figure 4: Kamoa plan map showing total copper grade for Indicated and Inferred Mineral Resources.

The area between the Resources (colored blocks) and model limit is considered to be the Exploration Target.

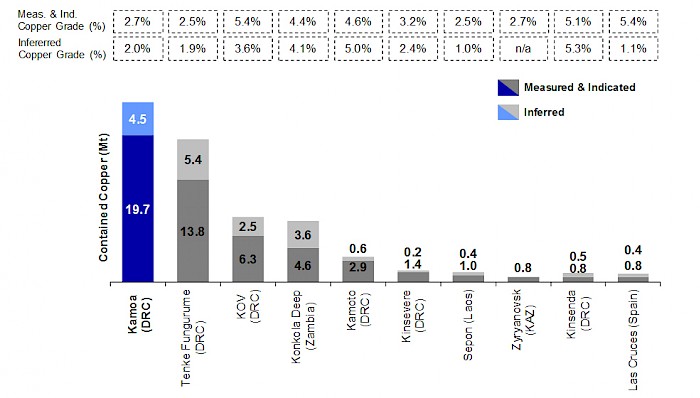

Figure 5: Contained copper in high-grade deposits (Measured & Indicated Mineral Resources, inclusive of Mineral Reserves, and Inferred Mineral Resources; with grades above 2.5% copper).

Source: Wood Mackenzie

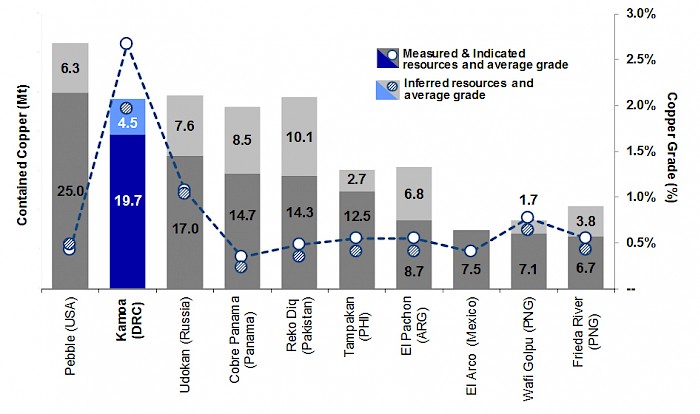

Figure 6: Contained copper in undeveloped deposits (Measured & Indicated Mineral Resources, inclusive of Mineral Reserves, and Inferred Mineral Resources).

Source: Wood Mackenzie

Focus of current drilling program

Ivanhoe is undertaking a drilling program that encompasses metallurgical, geotechnical, civil geotechnical and hydro-geological holes. Additional planned holes will be a combination of exploration, infill and delineation to target potential upgrades in Mineral Resource confidence categories and zones of additional mineralized material. The focus of this drilling will be down-dip expansion of the Kansoko trend, extension of the mineralization to the western extents of the mining licence and exploration drilling at Kakula for hypogene and shallow, open-pittable supergene targets.

Additional engineering drill holes, including metallurgical drilling, will be completed. Sterilization drilling using a Land Cruiser-mounted diamond-drill rig is planned. Drill holes that will target sources of aggregate for construction purposes also are planned.

Large-scale underground mining to use room-and-pillar and drift-and-fill methods

Given the favourable mining characteristics of the Kamoa Deposit as derived from the December 2012 mineral resource – including its relatively undeformed, continuous mineralization, local continuity between closely spaced drillholes and flat-to-moderate dips – it is considered amenable to large-scale, mechanized, room-and-pillar or drift-and-fill mining. The low dip and the flat, geometry of the resource make it conducive to room-and-pillar mining in the shallow portions of the deposit, transitioning to drift-and-fill mining in the deeper sections. These conventional mining methods are the accepted standards for mining deposits such as Kamoa.

A minimum mining thickness of 3.5 metres was used for the PEA. Any blocks less than 3.5 metres thick were diluted to 3.5 metres using the average grade of the adjacent hanging wall and footwall blocks. Room-and-pillar panels are designed to be 80 metres wide and 500 metres long, with in-panel extraction ratios ranging from 60%-80%, depending on the panel depth below surface. Partial extraction of the barrier pillars (up to 50%) is planned at the end of mining of each section. The overall extraction ratio in the room-and-pillar areas is expected to be between 56%-82%, depending on the depth below surface. Higher in-panel extraction ratios of up to 95% are expected within the drift-and-fill areas, with an overall extraction ratio of 85% after partial extraction of barrier pillars.

A strategy of prioritizing higher-grade mining areas early in the mine’s life, and then returning to the lower-grade areas later in the mine’s life, has been built into the mine plan.

Figure 7: Mining panel layout by mining section.

Source: Stantec

Infrastructure to support a 30-year mine plan

The mine infrastructure for the Kamoa Project has been designed to support a 30-year mine plan, which produces a total of 326 million tonnes to support an annual blister-copper production rate of 300,000 tonnes. The facility design incorporates early access to the Kansoko Sud and the southern portion of Kansoko Centrale, which are higher-grade areas within the deposit. Development of the Kamoa Sud access begins in Year 1 and provides access to Kamoa Sud, Kansoko Centrale and Kansoko Nord mining sections. Later in the mine’s life, at Year 16, as the production from the Kansoko Sud mining section is ramping down, production from the Kamoa Nord mining section is scheduled to begin.

The planned accesses to each mining section include a conveyor decline and two access declines. Additional infrastructure requirements, such as surface and underground offices, surface and underground maintenance facilities, ventilation raises and paste backfill plants, are designed to support operations at the blister-copper production rate of 300,000 tonnes per year.

Since the separation between the three portals ranges from 2.2 kilometres to 5.8 kilometres, each site will require separate infrastructures.

Development of the main access declines will be in mineralized material whenever possible, but some of the development will be in unmineralized waste.

Building of underground mine-access decline planned to begin early next year

Excavation of the first mine-access decline at Kansoko Sud is expected to begin early next year. The decline will provide access to high-grade, near-surface copper resources that are targeted for the planned first phase of production.

Metallurgical testwork and concentrator design

Circuit development work during 2011 to 2013 primarily was conducted at Xstrata Process Support (XPS) Laboratories in Sudbury, Ontario. A flow sheet was developed that was tailored to the fine-grained nature of the deposit. The circuit relied on a traditional mill-float-mill-float (MF2) approach to partially liberate particles, followed by fine regrinding of concentrates to achieve a concentrate grade suitable for smelting. Separate treatment of the primary and secondary rougher concentrates allowed for separately-optimized cleaner flotation of fast and slow species.

This configuration became known as the Milestone flow sheet and forms the basis of the Net Smelter Return (NSR) model and mine plan. The circuit was tested on various composites from across the resource and was able to achieve a recovery of 85.4% and a copper grade of 32.8% for hypogene material, and a recovery of 83.2% and copper grade of 45.1% for supergene material.

In the first half of 2013, the focus of development work shifted toward a reduction in the silica content of the final concentrate. Adjustments were made to the re-agent dosages, as well as the grinding media type, resulting in an improvement to 86.7% recovery at a 37.0% copper grade for hypogene material, and 82.9% recovery at a 51.4% copper grade for supergene material. Silica levels in the final concentrate also dropped from 19.1% to 13.1% for hypogene and from 26.0% to 18.1% for supergene.

Although these improvements were not realized in time to be incorporated into the mine plan and NSR, the updated hypogene results were incorporated into the design basis for the concentrator and smelter and form the basis of the PEA and associated economic results.

The concentrator is expected to be constructed in two phases and consists of a three million tonnes per year run-of-mine concentrator during the first four years of operation, followed by the commissioning of an additional eight million tonnes per year run-of-mine concentrator in Year 5.

The design incorporates a three-stage crushing circuit (underground primary crushing, run-of-mine stockpiling and secondary and tertiary crushing at the concentrator) to feed the primary mill-feed stockpile. The primary and secondary ball mills would operate in closed circuit with hydrocyclones. The flotation circuit would consist of primary and secondary rougher flotation, with a secondary grind stage located between the primary and secondary rougher flotation stages. The cleaner flotation circuit would consist of primary cleaners with scavengers and re-cleaners, and secondary cleaners with re-cleaners. The cleaner circuit would incorporate concentrate regrind stages for both the primary and secondary circuits. The final concentrate would be thickened before it is pumped to the concentrate filter(s).

During the initial years of production, the concentrate would be bagged in a bagging plant to facilitate transport. Following commissioning of the smelter, the concentrate filter cake would be conveyed to the smelter’s concentrate storage and blending area. The secondary rougher tails and multiple non-float streams from the secondary cleaner circuit report to the final tailings facility.

Smelter and acid plant details

The smelting process proposed in the PEA is based on the use of Direct-to-Blister flash smelting technology (DBF). For slag cleaning, a two-stage electric furnace process is applied. The smelter has a concentrate smelting capacity of 800,000 tonnes per year, which corresponds to a copper product capacity of 300,000 tonnes per year.

In the DBF concept, copper concentrate is processed by flash smelting to produce blister copper (approximately 98% copper) in a single smelting stage. Blister copper is transferred via launders to refining furnaces, after which it is cast as final product.

The function of the sulphuric-acid plant is to receive the SO2 and SO3 containing process gases from the direct-to-blister and refining furnaces and to produce concentrated sulphuric acid from these gases. The estimated average sulphuric-acid production is 1,600 tonnes per day and the estimated product quality is 98.5% sulphuric acid. A detailed marketing study has been carried out for the DRC’s Province of Katanga and the Zambian Copperbelt. The Congolese Copperbelt is a net acid-consuming area. The majority of the copper and cobalt in the area is in the form of copper or cobalt oxides, and a leach solvent extraction-electrowinning process is utilized to produce final product. This process consumes acid and a number of the operations on the Copperbelt run sulphur-burning acid plants to produce acid; others purchase acid from Zambia or from overseas. Operators in the DRC reportedly are paying US$300-$400 per tonne and prices have been up to $800 per tonne in previous years. It is estimated that the full production cost of producing sulphuric acid in a sulphur-burning acid plant in Katanga is approximately US$246 per tonne, excluding the capital cost of the sulphur-burning acid plant. For the purpose of the Kamoa PEA, a long-term acid credit of US$250 per tonne was used.

Agreement to ensure supply of electrical power from DRC grid

Power for the Kamoa Project is planned to be sourced from the DRC grid following the rehabilitation of three existing hydro power plants: Koni, Mwadingusha and Nzilo 1. A financing agreement between Ivanhoe Mines and DRC’s state-owned power company, La Société Nationale d’Electricité (SNEL), has been finalized and initialled by the two parties for the rehabilitation of these plants to secure a sustainable power supply to meet the requirements of Kamoa’s planned mine and smelter development. Kamoa will be powered by electricity from the national grid and on-site diesel generators until rehabilitation of the existing plants has been completed.

Qualified persons, quality control and assurance

The following companies have undertaken work in preparation of the PEA:

- AMC Consultants – Overall report preparation, open-pit potential and financial model.

- AMEC – Mineral Resource estimation.

- SRK Consulting – Mine geotechnical recommendations.

- Stantec Consulting International – Underground mine plan.

- Hatch – Process and infrastructure.

- Golder Associates Africa – Environmental, hydrology, hydrogeology, geochemistry and Tailings Storage Facility (TSF).

The independent qualified persons responsible for preparing the Kamoa Preliminary Economic Assessment are Bernard Peters, B. Eng. (AMC); Dr. Harry Parker (AMEC); Gordon Seibel (AMEC); Jarek Jakubec, C. Eng., (SRK); Mel Lawson, B. Eng. (Stantec); Arne Weissenberger, P.Eng. and Francois Marais, P.Eng. (Golder).

The scientific and technical information in this release has been reviewed and approved by Stephen Torr, P.Geo., Ivanhoe Mines’ Vice President, Project Geology and Evaluation, a Qualified Person under the terms of National Instrument 43-101. Mr. Torr has verified the technical data disclosed in this news release.

Data verification

AMEC reviewed the sample chain of custody, quality assurance and control procedures, and qualifications of analytical laboratories. AMEC is of the opinion that the procedures and QA/QC are acceptable to support Mineral Resource estimation. AMEC also audited the assay database, core logging, and geological interpretations on a number of occasions between 2009 and 2013 and found no material issues with the data as a result of these audits.

In the opinion of the AMEC QPs, the data verification programs undertaken on the data collected from the Kamoa Project support the geological interpretations, and the analytical and database quality and the data collected can support Mineral Resource estimation.

About Ivanhoe Mines

Ivanhoe Mines, with offices in Canada, the United Kingdom and South Africa, is advancing and developing its three principal projects:

- The Kamoa copper discovery in a previously unknown extension of the Central African Copperbelt in the DRC’s Province of Katanga.

- The Platreef Discovery of platinum, palladium, nickel, copper, gold and rhodium on the Northern Limb of the Bushveld Complex in South Africa.

- The historic, high-grade Kipushi zinc, copper and germanium mine, also on the Copperbelt in the DRC, that is being dewatered and upgraded to support a future return to production of copper, zinc and other metals following a care-and-maintenance program conducted between 1993 and 2011.

Ivanhoe Mines also is evaluating other opportunities as part of its objective to become a broadly based, international mining company.

Information contacts

Investors

Bill Trenaman +1.604.331.9834

Media

North America: Bob Williamson +1.604.512.4856

South Africa: Jeremy Michaels +27.11.088.4300

Website www.ivanhoemines.com

FORWARD-LOOKING STATEMENTS

Statements in this release that are forward-looking statements are subject to various risks and uncertainties concerning the specific factors disclosed here and elsewhere in the company’s periodic filings with Canadian securities regulators. When used in this document, the words such as “could,” “plan,” “estimate,” “expect,” “intend,” “may,” “potential,” “should” and similar expressions, are forward-looking statements. Information provided in this document is necessarily summarized and may not contain all available material information.

The results of the PEA represent forward-looking information. Statements in this release that constitute forward-looking statements or information include, but are not limited to: statements regarding the Kamoa mine is projected to have the highest grade among the world’s largest copper mines; statements regarding Kamoa to be one of the world’s lowest cost copper producers; statements regarding early cash flows from the sale of high-grade copper concentrate; statements regarding cash costs of US$1.18/lb of copper would rank Kamoa near the bottom of the global cash-cost curve; statements regarding estimated NPVs and IRRs; statements regarding the additional planned drilling in the current drill program; statements regarding mine infrastructure; statements regarding the excavation of the first mine-access decline at Kansoko Sud is expected to begin early next year; statements regarding metallurgical testwork and concentrator design; statements regarding planned smelter and acid plant; statements regarding the planned supply of electrical power.

The forward-looking information also includes metal price assumptions, cash flow forecasts, projected capital and operating costs, metal recoveries, mine life and production rates, and other assumptions used in the PEA. Readers are cautioned that actual results may vary from those presented. The factors and assumptions used to develop the forward-looking information, and the risks that could cause the actual results to differ materially are presented in the body of the Technical Report that will be filed on SEDAR at www.sedar.com and Ivanhoe Mines’ website at www.ivanhoemines.com within 45 days of this news release.

All such forward-looking information and statements are based on certain assumptions and analyses made by Ivanhoe Mines’ management in light of their experience and perception of historical trends, current conditions and expected future developments, as well as other factors management believes are appropriate in the circumstances. These statements, however, are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information or statements. Important factors that could cause actual results to differ from these forward-looking statements include those described under the heading “Risk Factors” in the company’s most recently filed MD&A. Readers are cautioned not to place undue reliance on forward-looking information or statements.