English

English Français

Français 日本語

日本語 中文

中文TORONTO, CANADA – Ivanhoe Mines (TSX: IVN) today announced its financial results for the first quarter ended March 31, 2016. All figures are in US dollars unless otherwise stated.

HIGHLIGHTS

- On May 11, 2016, Ivanhoe Mines announced a 58% increase in Indicated Mineral Resources tonnage and a 21% increase in Inferred Mineral Resources tonnage at its Platreef platinum-group metals, nickel, copper and gold project in South Africa.

- Platreef’s Indicated Resources now contain an estimated 42.0 million ounces of PGMs plus gold, with an additional 52.8 million ounces in Inferred Resources, at the base case cut-off grade of 2.0 grams/tonne (g/t) 3PE+gold.

- At a lower cut-off grade of 1.0 g/t 3PE+gold, Platreef’s Indicated Resources now contain an estimated 58.8 million ounces of PGMs plus gold, with an additional 94.3 million ounces in Inferred Resources.

- Main sinking at Platreef’s Shaft 1 is expected to begin in early June 2016. Aveng Mining, the shaft-sinking contractor, expects to sink at a daily average rate of approximately 2.5 metres. Shaft 1 is expected to reach the Flatreef Deposit at a depth of 777 metres below surface during the third quarter of 2017. Shaft 1 will provide early development access into the deposit and will be utilized to fast track production during the first phase of the project.

- On April 6, 2016, Ivanhoe announced that it was going to accelerate its drilling at the Kamoa Copper Project’s Kakula Discovery in the Democratic Republic of the Congo (DRC). Drilling will focus on the area surrounding the thick, high-grade intercepts reported in holes DD996 and DD997 announced in January 2016. Drilling initially will focus on a 12-square-kilometre area along the projected trend of mineralization intersected in holes DD996 and DD997. The drill program also includes follow-up infill drilling aimed at defining Indicated Resources in areas where the continuity of materially higher grade is confirmed.

- On February 23, 2016, Ivanhoe Mines reported the positive findings of an independent pre-feasibility study (PFS) for the first phase of development of the Kamoa Copper Project. The first phase envisages an annual production rate of three million tonnes of ore at an average grade of 3.86% copper over a 24-year mine life, resulting in annual copper production of approximately 100,000 tonnes. Initial capital costs, including contingency, are estimated at $1.2 billion, approximately $200 million lower than estimated in the Kamoa 2013 preliminary economic assessment.

- Construction work on the twin declines at Kamoa began in March 2016. The declines are designed to intersect the high-grade copper mineralization in the initial mining area at Kansoko Sud, approximately 150 metres below surface. Ivanhoe’s drilling program in this area defined a thick, near-surface zone of high-grade copper mineralization, where a drill hole intercepted 15.7 metres (true width) of 7.04% copper. Byrnecut Underground Congo is the contractor for the permanent support of the box-cut walls and the initial 1.2 kilometres of development for each of the two declines.

- Also in the DRC, on May 2, 2016, Ivanhoe Mines announced a positive preliminary economic assessment (PEA) for the redevelopment of the Kipushi zinc-copper-germanium-lead-silver mine. The PEA plan covers the redevelopment of Kipushi as an underground mine, producing an average of 530,000 tonnes of zinc concentrate annually over a 10-year mine life at a total cash cost, including copper by-product credits, of approximately $0.54 per pound of zinc. Successful planned restoration of production would make Kipushi the world’s highest grade, major zinc mine.

- On January 27, 2016, Ivanhoe Mines announced receipt of a new, independent, Mineral Resource estimate for Kipushi. Kipushi’s Big Zinc Zone is estimated to contain Measured and Indicated Mineral Resources of 10.2 million tonnes at 34.9% zinc, containing 7.8 billion pounds of zinc. This grade is more than twice as high as the Measured and Indicated Mineral Resources of the world’s next-highest-grade zinc project, according to Wood Mackenzie, a leading, international industry research and consulting group. Adjacent zones of copper-rich mineralization contain estimated Measured and Indicated Mineral Resources of 1.6 million tonnes at 4.01% copper, containing 144 million pounds of copper.

- Leveraging existing surface and underground infrastructure at Kipushi is expected to significantly lower the redevelopment capital compared to a greenfield development project and also reduce the time required to reinstate production. The after-tax project payback period is 2.2 years and the after-tax internal rate of return is 30.9%.

- Ivanhoe Mine’s three projects achieved a combined 10 million hours of lost-time-injury-free (LTIF) work by the end of the first quarter of 2016. Ivanhoe had recorded 0.9 million LTIF hours at Platreef, 4.8 million hours at Kamoa and 4.3 million hours at Kipushi to the end of Q1 2016.

Principal Projects and Review of Activities

1. Platreef Project

64%-owned by Ivanhoe Mines

South Africa

The Platreef Project is owned by Ivanplats (Pty.) Ltd., which is 64%-owned by Ivanhoe Mines. A 26% interest is held by Ivanplats’ broad-based, black economic empowerment partners, which include 20 local host communities with a total of approximately 150,000 people, historically-disadvantaged project employees and local entrepreneurs. Ivanplats reconfirmed its Level 3 status in its second verification assessment on a B-BBEE scorecard. A Japanese consortium of ITOCHU Corporation and its affiliate, ITC Platinum, plus Japan Oil, Gas and Metals National Corporation and JGC Corporation, owns a 10% interest in Ivanplats, which it acquired in two tranches for a total investment of $290 million.

The Platreef Project hosts an underground deposit of thick, platinum-group metals, nickel, copper and gold mineralization in the Northern Limb of the Bushveld Igneous Complex, approximately 280 kilometres northeast of Johannesburg and eight kilometres from the town of Mokopane in Limpopo Province. Since 2007, Ivanhoe has focused its exploration activities on defining and advancing the down-dip extension of its original Platreef discovery, now known as the Flatreef Deposit, which is amenable to highly mechanized, underground mining methods. The Flatreef area lies entirely on the Turfspruit and Macalacaskop properties, which form part of the company’s mining right.

South Africa’s new draft Mining Charter

On April 15, 2016, the South African Government’s Department of Mineral Resources published a draft revision of the Mining Charter for public comment. The draft is likely to be amended following negotiations between the Government and various stakeholders, including the mining industry.

It would be inappropriate to speculate at this stage about the extent to which the draft Mining Charter will be changed. However, if the draft Mining Charter were to be enforced in its current form, Ivanhoe is confident that it either would be compliant already, in relation to the majority of the revised compliance targets, and/or be able to achieve the revised compliance targets within the transitional period of three years postulated in the draft.

Updated Mineral Resource Estimate results in substantial increase in Indicated and Inferred Mineral Resources at Platreef

On May 11, 2016, Ivanhoe Mines issued a news release announcing a substantial increase in Indicated and Inferred Mineral Resources at the company’s Platreef Project. The updated Mineral Resource estimate was prepared by Ivanhoe Mines under the direction of Dr. Harry Parker, RM SME of Amec Foster Wheeler E&C Services Inc (Amec Foster Wheeler). Dr. Parker and Mr. Timothy Kuhl RM SME, also of Amec Foster Wheeler, have independently confirmed the Mineral Resource estimate and are the Qualified Persons for the estimate, which has an effective date of April 22, 2016

Highlights of the updated Platreef Project Mineral Resource estimate, reported on a project basis in which Ivanhoe has an attributable 64% interest, include:

- An increase of 58% in the Indicated Mineral Resources tonnage to 346 million tonnes, at a grade of 3.77 grams per tonne (g/t) platinum, palladium, rhodium plus gold (3PE+Au), 0.32% nickel and 0.16% copper, at a cut-off grade of 2.0 grams/tonne (g/t) 3PE+Au.

- An increase of 21% in the Inferred Mineral Resources tonnage to 506 million tonnes, at a grade of 3.24 g/t 3PE+Au, 0.31% nickel and 0.16% copper, at a cut-off grade of 2.0 g/t 3PE+Au.

- An increase of 45% in the contained metal in Indicated Mineral Resources, at a cut-off grade of 2.0 g/t 3PE+Au, totalling 41.95 million ounces of 3PE+Au, plus a 47% increase in nickel to 2.44 billion pounds and a 50% increase in copper to 1.23 billion pounds.

- Contained metal in Inferred Mineral Resources, at a cut-off grade of 2.0 g/t 3PE+Au, has increased by 11% to total 52.77 million ounces of 3PE+Au, nickel has increased by 13% to total 3.44 billion pounds and copper has increased by 18% to 1.78 billion pounds.

- An average thickness of 19 metres in the area of the TCU-T2 mineralized zone where Indicated Mineral Resources are estimated and an average thickness of 12.7 metres for the area where Inferred Mineral Resources are estimated, using the 2.0 g/t 3PE+Au cut-off.

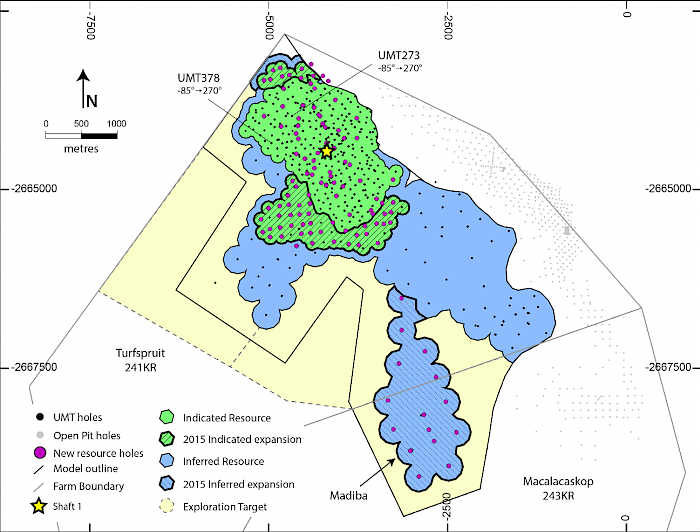

The substantial increase in the Platreef Project’s Indicated and Inferred Mineral Resources in the updated 2016 estimate results primarily from the additional 97,737 metres of detailed infill and exploration drilling that was completed between August 2012 and February 2015. A plan view of the additional drilling is shown in Figure 1.

The increase also is driven by a revised and improved geological interpretation by Ivanhoe’s geologists, with additional Mineral Resources now estimated in areas that were drilled before 2013. Since the February 2013 Mineral Resource estimate, Ivanhoe’s geologists have completed relogging of cores and an updated geological interpretation of the entire portion of the Platreef Project amenable to underground mining. The result is estimation of Mineral Resources amenable to selective mining in areas previously categorized as being amenable only to bulk-mining methods.

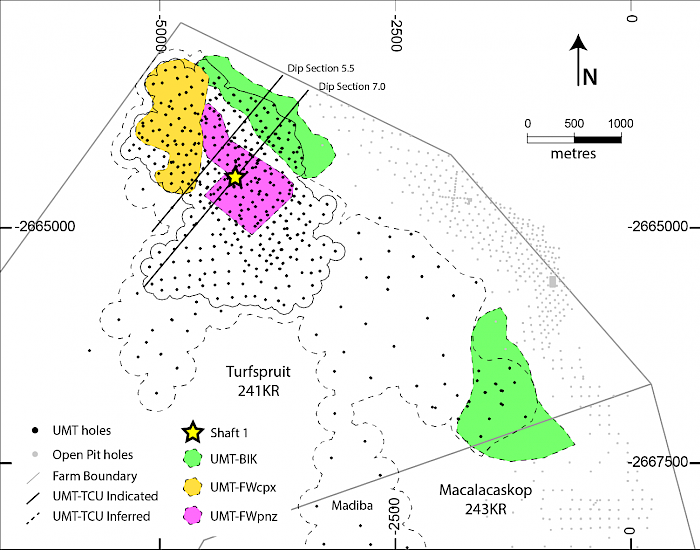

The consolidated Mineral Resources for the Platreef Project now include Bikkuri Mineral Resources (UMT-BIK) and additional mineralized zones in the footwall of the key mineralized zone, the TCU, referred to collectively as the UMT-FW Mineral Resources. The consolidated Mineral Resources for the Platreef Project are shown in Table 1 (2.0 g/t 3PE+Au base case highlighted). The UMT-FW consists of two zones, the FWcpx and FWpnz. The location of the various mineralized zones (Resource Areas) in a plan view is shown in Figure 2.

The Mineral Resource is presented on a 100% project basis, with the company having an attributable interest of 64%.

Table 1: Platreef Mineral Resource – all mineralized zones (2.0 g/t 3PE+Au is the base case).

| Indicated Mineral Resources – Tonnage and Grades | ||||||||

|---|---|---|---|---|---|---|---|---|

| Cut-off Grade (3PE+Au) | Mt | Pt (g/t) | Pd (g/t) | Au (g/t) | Rh (g/t) | 3PE+Au (g/t) | Cu (%) | Ni (%) |

| 3.0 g/t | 204 | 2.11 | 2.11 | 0.34 | 0.14 | 4.7 | 0.18 | 0.35 |

| 2.0 g/t | 346 | 1.68 | 1.70 | 0.28 | 0.11 | 3.77 | 0.16 | 0.32 |

| 1.0 g/t | 716 | 1.11 | 1.16 | 0.19 | 0.08 | 2.55 | 0.13 | 0.26 |

| Indicated Mineral Resources – Contained Metal | ||||||||

| Cut-off Grade (3PE+Au) | Pt (Moz) | Pd (Moz) | Au (Moz) | Rh (Moz) | 3PE+Au (Moz) | Cu (Mlbs) | Ni (Mlbs) | |

| 3.0 g/t | 13.86 | 13.86 | 2.23 | 0.92 | 30.86 | 800 | 1,597 | |

| 2.0 g/t | 18.66 | 18.94 | 3.12 | 1.23 | 41.95 | 1,226 | 2,438 | |

| 1.0 g/t | 25.63 | 26.81 | 4.49 | 1.82 | 58.75 | 2,076 | 4,108 | |

| Inferred Mineral Resources – Tonnage and Grades | ||||||||

| Cut-off Grade (3PE+Au) | Mt | Pt (g/t) | Pd (g/t) | Au (g/t) | Rh (g/t) | 3PE+Au (g/t) | Cu (%) | Ni (%) |

| 3.0 g/t | 225 | 1.91 | 1.93 | 0.32 | 0.13 | 4.29 | 0.17 | 0.35 |

| 2.0 g/t | 506 | 1.42 | 1.46 | 0.26 | 0.10 | 3.24 | 0.16 | 0.31 |

| 1.0 g/t | 1431 | 0.88 | 0.94 | 0.17 | 0.07 | 2.05 | 0.13 | 0.25 |

| Inferred Mineral Resources – Contained Metal | ||||||||

| Cut-off Grade (3PE+Au) | Pt (Moz) | Pd (Moz) | Au (Moz) | Rh (Moz) | 3PE+Au (Moz) | Cu (Mlbs) | Ni (Mlbs) | |

| 3.0 g/t | 13.78 | 13.96 | 2.33 | 0.94 | 31.01 | 865 | 1,736 | |

| 2.0 g/t | 23.17 | 23.78 | 4.26 | 1.56 | 52.77 | 1,775 | 3,440 | |

| 1.0 g/t | 40.38 | 43.01 | 7.81 | 3.06 | 94.27 | 4,129 | 7,759 | |

- Mineral Resources have an effective date of April 22, 2016. The Qualified Persons for the estimate are Dr. Harry Parker, RM SME, and Timothy Kuhl, RM SME, who are employees of Amec Foster Wheeler E&C Services Inc. and independent of Ivanhoe. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

- The 2 g/t 3PE+Au cut-off is considered the base case estimate and is highlighted. The rows are not additive.

- Mineral Resources are reported on a 100% basis. Mineral Resources are stated from approximately -200 m to 650 m elevation (from 500 m to 1,350 m depth). Indicated Mineral Resources are drilled on approximately 100 x 100 m spacing (locally 150 m spacing); Inferred Mineral Resources are drilled on 400 x 400 m (locally to 400 x 200 m and 200 x 200 m) spacing.

- Mineral Resources have been estimated on an externally undiluted basis and without consideration for mining recovery. Dilution and mining recoveries will vary with the geometry (dip, thickness, faulting and or irregularities in contacts) of the mineralization and the eventual mining method used.

- Reasonable prospects for eventual economic extraction were determined using the following assumptions. Assumed commodity prices are Pt: $1,600/oz, Pd: $815/oz, Au: $1,300/oz, Rh: $1,500/oz, Cu: $3.00/lb and Ni: $8.90/lb. It has been assumed that payable metals would be 82% from smelter/refinery and that mining costs (average $34.27/t) and process, G&A, and concentrate transport costs (average $15.83/t of mill feed for a 4 Mtpa operation) would be covered. The processing recoveries vary with block grade but typically would be 80%–90% for Pt, Pd and Rh; 70-90% for Au, 60-90% for Cu, and 65-75% for Ni.

- 3PE+Au = Pt + Pd + Rh + Au.

- Totals may not sum due to rounding.

The Flatreef Mineral Resource, with a strike length of 6.5 kilometres, lies predominantly within a flat-to-gently-dipping portion of the Platreef mineralized belt at relatively shallow depths of approximately 500 metres to 1,350 metres below the surface.

The Flatreef Deposit is characterized by its very large vertical thicknesses of high-grade mineralization and a platinum-to-palladium ratio of approximately 1:1, which is significantly higher than other recent PGM discoveries on the Bushveld’s Northern Limb.

Figure 1: Platreef’s Indicated Resources shown in green; Inferred Resources in blue; areas of resource expansion indicated with diagonal lines; exploration target areas in beige.

Figure 2: Plan view showing the location of the new resource areas relative to Shaft 1. Bikkuri Mineral Resources (UMT-BIK) is shown in green; the two separate domains of Footwall Mineral Resources (UMT-FW) are shown in orange (UMT-FWcpx) and purple (UMT-FWpnz).

Potential for additional UMT-TCU mineralization within targets for further exploration

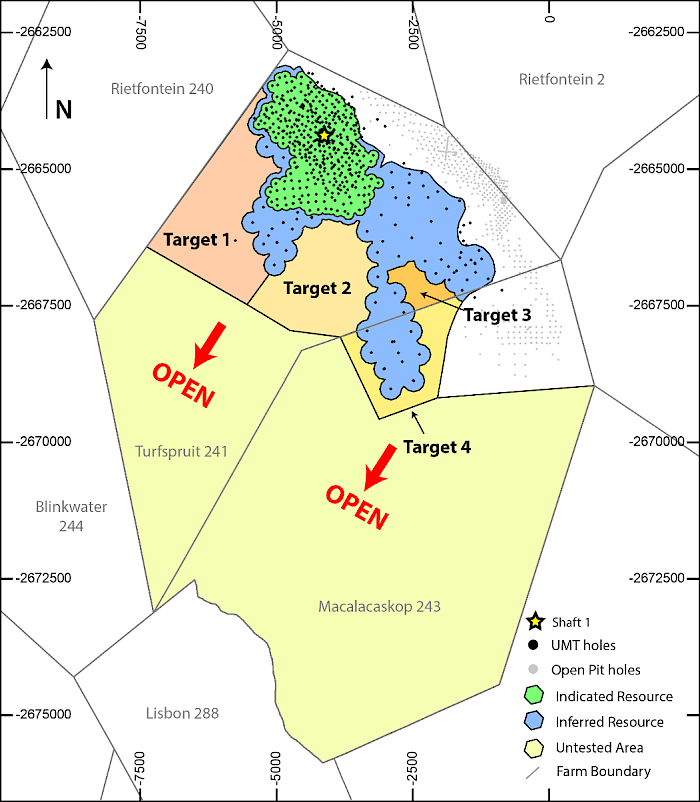

Exploration potential exists immediately outside the area of Inferred Mineral Resources that has not been explored by Ivanhoe. Amec Foster Wheeler has defined four targets for further exploration (exploration targets) in areas that are contiguous with the current Mineral Resource areas that are shown in Figure 3.

Target 1 could contain 150 to 250 million tonnes grading 1.2 to 1.9 g/t Pt, 1.2 to 1.9 g/t Pd, 0.19 to 0.32 g/t Au, 0.08 to 0.14 g/t Rh, (2.6 to 4.3 g/t 3PE+Au), 0.11 to 0.19% Cu and 0.23 to 0.38% Ni over an area of 4.1 km2. The tonnage and grades are based on intersections of 2.0 g/t 3PE+Au mineralization in drill holes located adjacent to the target.

Target 2 could contain 50 to 90 million tonnes grading 1.3 to 2.1 g/t Pt, 1.4 to 2.3 g/t Pd, 0.19 to 0.31 g/t Au, 0.11 to 0.18 g/t Rh, (2.9 to 4.9 g/t 3PE+Au), 0.11 to 0.19% Cu and 0.23 to 0.39% Ni over an area of 3.9 km2. The tonnage and grades are based on intersections of 2.0 g/t 3PE+Au mineralization in drill holes located adjacent to the target.

Target 3 could contain 5 to 10 million tonnes grading 1.3 to 2.2 g/t Pt, 1.1 to 1.9 g/t Pd, 0.20 to 0.34 g/t Au, 0.10 to 0.17 g/t Rh, ( 2.7 to 4.6 g/t 3PE+Au), 0.11 to 0.18% Cu and 0.23 to 0.38% Ni over an area of 0.5 km2. The tonnage and grades are based on intersections of 2.0 g/t 3PE+Au mineralization in drill holes located adjacent to the target.

Target 4 could contain 40 to 60 million tonnes grading 1.3 to 2.2 g/t Pt, 1.5 to 2.5 g/t Pd, 0.18 to 0.30 g/t Au, 0.12 to 0.20 g/t Rh, (3.1 to 5.2 g/t 3PE+Au), 0.10 to 0.17% Cu and 0.22 to 0.36% Ni over an area of 1.5 km2. The tonnage and grades are based on intersections of 2.0 g/t 3PE+Au mineralization in drill holes located adjacent to the target.

The potential quantity and grade of these exploration targets is conceptual in nature. There has been insufficient exploration and/or study to define these exploration targets as Mineral Resources. It is uncertain if additional exploration will result in these exploration targets being delineated as a Mineral Resource.

In addition, there are approximately 48 km2 of unexplored ground beyond these exploration target areas on the property under which the prospective stratigraphy is projected to lie. It is not possible to estimate a range of tonnages and grades for this ground with current information. There is excellent potential for mineralization to significantly increase with further step-out drilling to the southwest.

Figure 3: Mineralization at the Platreef Project is open to expansion to the south and west, beyond the area of the current Indicated Mineral Resources shown in green, and the Inferred Mineral Resources, shown in blue.

Health and safety at Platreef

The Platreef Project reached 5,505,507 million hours worked by March 30, 2016. The project recorded 873,461 lost-time-injury-free (LTIF) hours at Platreef up until the end of Q1 2016. No lost-time injuries (LTIs) were recorded in the reporting period and the Platreef Project continues to strive toward its workplace objective of an environment that causes zero harm to employees, contractors, sub-contractors and consultants.

Shaft 1 construction

Following the changeover from the pre-sinking phase, the main sinking work at Shaft 1 is expected to begin in early June 2016. Aveng Mining, the shaft-sinking contractor, expects sinking to advance at an average daily rate of approximately 2.5 metres once the main sink has commenced. Shaft 1 is expected to reach the Flatreef Deposit at a depth of 777 metres below surface by late 2017. Sinking will continue to a planned final depth of 975 metres below surface. Development work will include three stations at depths of 450 metres, 750 metres and 850 metres below surface.

Work has been completed on the internal electricity substation, which will have a capacity of five million volt-amperes (MVA). Construction is underway on the power transmission lines from Eskom, the South African public electricity utility, which will supply the electrical power to be used for the sinking of Shaft 1. Back-up generators have been installed to ensure continuous sinking operations if the power supply from Eskom is interrupted and will be utilized while construction of the powerlines is in progress.

Platreef implementing a phased approach to a large, underground, mechanized mine

Ivanhoe completed a pre-feasibility study (PFS) in January 2015 that covered the first phase of development that is expected to include construction of an underground mine, concentrator and other associated infrastructure.

In August 2015, Ivanhoe started work on a feasibility study (FS) based on the first phase of development. The FS is being managed by principal consultant, DRA Global, with other specialized sub-consultants including Stantec Consulting, Murray & Roberts Cementation, SRK, Golder Associates and Digby Wells Environmental. The FS is scheduled to be completed by Q2 2017.

There will be opportunities to refine and modify the timing and capacities of subsequent phases of production to suit market conditions during the development and commissioning of the first phase.

Platreef PFS highlights

- Development of a large, mechanized, underground mine with an initial four-million-tonne-per-year concentrator and associated infrastructure.

- Planned initial average annual production rate of 433,000 ounces of platinum, palladium, rhodium and gold (3PE+Au), plus 19 million pounds of nickel and 12 million pounds of copper.

- Estimated pre-production capital requirement of approximately $1.2 billion, including $114 million in contingencies, at a ZAR:USD exchange rate of 11 to 1.

- Platreef would rank at the bottom of the cash-cost curve, at an estimated $322 per ounce of 3PE+Au, net of by-products.

- The planned Platreef mine is projected to require a workforce of approximately 2,200 within four years of the start of production.

- After-Tax Net Present Value (NPV) of $972 million, at an 8% discount rate.

- After-Tax Internal Rate of Return (IRR) of 13%.

The development scenarios describe a staged approach structured to provide opportunities to expand the operation based on demand, smelting and refining capacity and capital availability.

Metallurgical testwork and processing

Metallurgical testwork has focused on maximizing the recovery of platinum-group elements (PGE) and base metals, while producing an acceptably high-grade concentrate suitable for further processing and/or sale to a third party. The three main geo-metallurgical units and composites have produced smelter-grade final concentrates of approximately 85 g/t 3PE + gold at acceptable PGE recoveries. Testwork also has shown that the material is amenable to treatment by one stage of mainstream grinding followed by conventional flotation, without the need for concentrate re-grinding. Batch open-circuit and locked-cycle flotation testwork has been performed.

A two-phased development approach was used for PFS flow-sheet design. The selected flow sheet is comprised of a four-million-tonne-per-year, three-stage crushing circuit that will feed crushed material to two parallel milling-flotation modules, each with a capacity of two million tonnes per year. Flotation is followed by a four-million-tonne-per-year tailings-handling and concentrate-thickening, filtration and storage circuit.

Planned mining methods to incorporate highly productive, mechanized methods

The selected mining areas in the current mine plan occur at depths ranging from approximately 700 metres to 1,200 metres below the surface. The main access to the Flatreef Deposit and ventilation system is expected to be comprised of four vertical shafts. Shaft 2 will host the main personnel transport cage, material and ore-handling systems, while Shafts 1, 3 and 4 will be utilized for ventilation to the underground workings. Shaft 1, now under development, will be used for initial access to the deposit and early underground development.

Mining will be performed using highly productive, mechanized methods, including long-hole stoping, drift-and-bench and drift-and-fill mining methods. The mined-out areas within the deposit will be backfilled with a paste mixture that utilizes tailings from the process plant and cement. The ore will be hauled from the stopes to a series of ore passes that connect to a main haulage level, which will be connected to Shaft 2, where it will be hoisted to the surface for further processing.

Shaft 1 will have an internal diameter of 7.25 metres. It is projected to intersect the Flatreef deposit at a depth of 777 metres below surface in late 2017 and reach its total depth of 975 metres in 2018.

Shaft 2 will have an internal diameter of 10.0 metres and will be capable of hoisting six million tonnes per year. The headgear design for the six-million-tonne-per-year permanent hoisting facility has been completed by South Africa-based Murray & Roberts Cementation. Ivanhoe expects to start Shaft 2 early works in 2017, including civil work for the box-cut and hitch-foundation.

Bulk water and electricity supply

The Olifants River Water Resource Development Project (ORWRDP) is designed to deliver water to the Eastern and Northern limbs of South Africa’s Bushveld Igneous Complex. The project consists of the new De Hoop Dam, the raised wall of the Flag Boshielo Dam and related pipeline infrastructure that ultimately will deliver water to Pruissen, southeast of the Northern Limb. The Pruissen Pipeline Project will be developed to deliver water onward from Pruissen to the municipalities, communities and mining projects on the Northern Limb. Ivanhoe is a member of the ORWRDP’s Joint Water Forum. The Minister of Water & Sanitation has directed that the Trans-Caledon Tunnel Authority will serve as the implementing agent for the outstanding phases of the ORWRDP scheme, which include the Phase 2B pipeline from Flag Boshielo Dam to Mokopane.

Participants in the water development scheme are required to indicate their water requirements so that the total water demand may be calculated relative to the scheme’s capacity. The Platreef Project’s water requirement for the first phase of development is projected to peak at approximately 10 million litres per day. Ivanhoe also is continuing to investigate various alternative bulk water sources, including bulk grey water allocations from local municipalities.

The Platreef Project’s electricity requirement for a four-million-tonne-per-year underground mine, concentrator and associated infrastructure has been estimated at approximately 100 million volt-amperes (MVA). As power is required for the initial mine development work, including shaft sinking, before the main power supply becomes available, an agreement with Eskom has been reached for the supply of 5MVA of temporary construction power. Ivanhoe opted for a self-build option for the permanent power, which enables Ivanhoe to manage the construction of the distribution lines from the Eskom Borutho sub-station to the Platreef Mine.

Development of human resource and job skills

Work is progressing well on the further implementation of Ivanhoe’s Social and Labour Plan (SLP), to which the company has pledged a total of R160 million ($11 million) during the first five years, until November 2019. The approved plan includes R67 million ($4 million) for the development of job skills among local residents and R88 million ($6 million) for local economic development projects. Additional internal training is planned to provide members of the current workforce with opportunities to expand their skills.

Adult basic education and training for the communities is progressing well in four community centres run by the Department of Higher Education and Training, further forging a partnership between Ivanhoe and the Department.

The first 80 students to participate in Platreef’s non-core training program started their training at the beginning of March 2016. Additional related training programs are planned later in the year.

Ivanhoe awarded five fully-paid bursaries to local university students in 2015. To date in 2016, Ivanhoe has awarded fully-paid bursaries to seven local university students in diverse disciplines. In addition, Ivanhoe also is developing local artisans with the establishment of fully paid engineering scholarships.

Ivanhoe’s R24 million ($2 million) partnership between South Africa’s University of Limpopo and Canada’s Laurentian University to develop and equip Limpopo University’s geology department is well underway. A principal goal of the five-year partnership, which is renewable for a further five years, is to help establish the University of Limpopo’s geology department as a centre of excellence in geosciences. Combined with a scholarship awarded to Laurentian by the International Development Research Centre, these funds will create educational opportunities for 35 University of Limpopo students to study in Canada. Ivanhoe also will provide in-service training opportunities for students from both universities and assist them in conducting research on the Northern Limb of the Bushveld Complex.

As part of Ivanhoe’s commitment to provide expanded work opportunities, 2016 will see the launch of the first Youth Development Program. Young people from the local communities, aged between 21 and 32, will be enrolled in a development course that will work toward a final product of a bankable business plan to be submitted for funding.

2. Kipushi Project

68%-owned by Ivanhoe Mines

Democratic Republic of Congo (DRC)

The Kipushi copper-zinc-germanium-lead mine, in the Democratic Republic of Congo (DRC), is adjacent to the town of Kipushi and approximately 30 kilometres southwest of Lubumbashi. It also is located on the Central African Copperbelt, approximately 250 kilometres southeast of Ivanhoe’s Kamoa Project, and less than one kilometre from the Zambian border. Ivanhoe acquired its 68% interest in the Kipushi Project in November 2011; the balance of 32% is held by the state-owned mining company, La Générale des Carrières et des Mines (Gécamines).

Health, safety and community development at Kipushi

The Kipushi Project achieved a total of 4,260,651 lost-time-injury-free hours (1,333 days) to the end of Q1 2016. Malaria remains the most frequent health concern at Kipushi; in Q1 2016, there was an average of 17 cases each month among employees, which is the seasonal peak at the end of the rainy season.

In an effort to reduce the incidence of malaria in the Kipushi community, a Water Sanitation and Health (WASH) program has been initiated in cooperation with the Territorial Administrator and the local community. The main emphasis in the program’s first phase is cleaning storm drains in the municipality to prevent the accumulation of ponded water, where malarial mosquitos breed.

Following DRC government approval of the Fionet program, training of medical staff at medical service providers in the Kipushi Health Zone on the use of the Deki™rapid malaria test reader started in December 2015 and will continue on an ongoing basis. The objective is to establish the Fionet program in 37 medical centres in the Kipushi Health Zone. The program eventually will be rolled out to 300 clinics in the Haut-Katanga province. To date, 37 Deki readers have been installed, and local medical staff trained, in the Kipushi Health Zone.

As part of the Kipushi municipality development program, Ivanhoe has contracted Mining Company Katanga (MCK) to repair the main road through the community, which has been damaged by rain erosion and heavy traffic over many years.

Project development and infrastructure

The mine, which had been placed on care and maintenance in 1993, flooded in early 2011 due to a lack of pump maintenance over an extended period. At its peak, water reached 851 metres below the surface level. A major milestone was reached in December 2013 when Ivanhoe restored access to the mine’s principal haulage level at 1,150 metres below the surface. Since then, crews have been upgrading underground infrastructure to permanently stabilize the water levels.

A Mineral Resource estimate has been declared and the findings of a preliminary economic assessment (PEA) for the Kipushi Project were announced on May 2, 2016.

Since completion of the drilling program, water levels have been lowered to approximately the 1,400-metre-level in Shaft 5. Engineering work has focussed on refurbishment of Shaft 5 conveyances and infrastructure, cleaning of the shaft bottom to facilitate the installation of new hoist ropes, repairs and upgrades to the hoisting infrastructure and cleaning and stripping of the main pump station at the 1,200-metre-level.

Replacing wire rope on Shaft 5 personnel cage using the friction winder.

Sulzer centrifugal pump on the 1,200-metre-level pump station.

Y junction on 1,200-metre-level, personnel cage to left, ore silos to right.

Environmental studies

Golder Associates was engaged in early 2014 to conduct an International Finance Corporation-compliant Environmental, Social and Health Impact Assessment (ESHIA) baseline study to determine the impact of previous mining activities by Gécamines and provide a baseline for the future. Sampling of mine discharge, ground and surface water and air quality is ongoing to meet regulatory requirements.

Current sustainability programs include the continued maintenance and operation of the potable-water pump station and well field supplying the Kipushi municipality, logistical support to the Kipushi Health Zone and small-animal husbandry programs.

Independent Mineral Resource estimate

Ivanhoe announced a Mineral Resource estimate for Kipushi on January 27, 2016. The estimate was prepared in accordance with the 2014 CIM definition standards, incorporated by reference into Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

Highlights of the initial estimate, prepared by the MSA Group, of Johannesburg, South Africa:

- Measured and Indicated Mineral Resources in the Big Zinc Zone of 10.2 million tonnes at grades of 34.89% zinc, 0.65% copper, 19 grams per tonne (g/t) silver and 51 g/t germanium, at a 7% zinc cut-off, containing an estimated 7.8 billion pounds of zinc.

- The zinc grade of Kipushi’s Measured and Indicated Mineral Resources in the Big Zinc Zone is more than twice as high as the world’s next-highest-grade zinc project, independently ranked by Wood Mackenzie, an international industry research and consulting group, based on contained zinc.

- Zinc-rich Inferred Mineral Resources total an additional 1.9 million tonnes at grades of 28.24% zinc, 1.18% copper, 10 g/t silver and 53 g/t germanium. The Inferred Mineral Resources are contained partially in the Big Zinc Zone and partially in the Southern Zinc Zone.

- Kipushi’s copper-rich Measured and Indicated Mineral Resources contained in the adjacent Fault Zone, Fault Zone Splay and Série Récurrente Zone total an additional 1.63 million tonnes at grades of 4.01% copper, 2.87% zinc and 22 g/t silver, at a 1.5% copper cut-off, containing 144 million pounds of copper. Copper-rich Inferred Mineral Resources in these zones total an additional 1.64 million tonnes at grades of 3.30% copper, 6.97% zinc and 19 g/t silver.

- Ivanhoe’s exploration program has demonstrated that zinc and copper mineralization of the Kipushi system remains open laterally and at depth. Results recently received from hole KPU081, drilled on section line 6S, confirm high-grade copper-zinc mineralization at depth. KPU081 intersected 60.5 metres (21.7 metres true thickness) grading 2.6% copper, 36.2% zinc, 19 g/t silver and 204 g/t germanium to a depth of 1,763 metres. Included in this interval was an intersection from 580.9 metres to 591.3 metres (3.8 metres true thickness) grading 56.3% zinc, 0.5% copper, 12 g/t silver and 397 g/t germanium.

The MSA Mineral Resource estimate was based on the results of 84 drill holes completed at Kipushi by Ivanhoe Mines and an additional 107 historical holes drilled by Gécamines. Mineral Resource estimates were completed below the -1,150-metre-level on the Big Zinc Zone, Southern Zinc Zone, Fault Zone and Série Récurrente Zone. The Mineral Resources were categorized either as zinc-rich resources or copper-rich resources, depending on the most abundant metal.

For the zinc-rich zones, the Mineral Resource is reported at a base-case cut-off grade of 7.0% zinc and the copper-rich zones at a base-case cut-off grade of 1.5% copper. Given the considerable revenue that could be obtained from the additional metals in each zone, MSA considers that mineralization at these cut-off grades will satisfy reasonable prospects for economic extraction.

The Mineral Resource is presented on a 100% project basis, with the attributable interest of the company being 68%.

Preliminary Economic Assessment announced for the redevelopment of the Kipushi Project

Ivanhoe announced a positive preliminary economic assessment (PEA) for the redevelopment of the Kipushi Project on May 2, 2016. The PEA was prepared in compliance with Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects. Ivanhoe will file a NI 43-101 Technical Report on the PEA within 45 days of the announcement.

Highlights of the PEA, prepared by OreWin Pty. Ltd., of Adelaide, Australia, and the MSA Group (Pty.) Ltd., of Johannesburg, South Africa include:

- After-tax net present value (NPV) at an 8% real discount rate is $533 million.

- After-tax real internal rate of return (IRR) is 30.9%.

- After-tax project payback period is 2.2 years.

- Leveraging existing surface and underground infrastructure significantly lowers the redevelopment capital compared to a greenfield development project, as well as the time required to reinstate production.

- Life-of-mine average planned zinc concentrate production of 530,000 dry tonnes per annum (tpa), with a concentrate grade of 53% zinc, is expected to rank Kipushi, once in production, among the world’s major zinc mines.

- Life-of-mine average cash cost of $0.54/lb of zinc is expected to rank Kipushi, once in production, in the bottom quartile of the cash cost curve for zinc producers globally.

3. Kamoa Project

47%-owned by Ivanhoe Mines

Democratic Republic of Congo (DRC)

The Kamoa Copper Project, a joint venture between Ivanhoe Mines and Zijin Mining, is a very large, stratiform copper deposit with adjacent prospective exploration areas within the Central African Copperbelt, approximately 25 kilometres west of the town of Kolwezi and about 270 kilometres west of Lubumbashi. Ivanhoe sold a 49.5% share interest in Kamoa Holding Limited (Kamoa Holding), the company that presently owns 95% of the Kamoa Project, to Zijin Mining for an aggregate consideration of $412 million. In addition, Ivanhoe sold a 1% share interest in Kamoa Holding to privately-owned Crystal River Global Limited for $8.32 million – which Crystal River will pay through a non-interest-bearing, 10-year promissory note.

A 5%, non-dilutable interest in the Kamoa Project was transferred to the DRC government on September 11, 2012, for no consideration, pursuant to the DRC Mining Code. Ivanhoe also has offered to transfer an additional 15% interest to the DRC government on terms to be negotiated. Constructive and cordial negotiations over the offer are continuing between Ivanhoe Mines, Zijin and senior DRC government officials. Subsequent to the sale to Zijin and Crystal River, Ivanhoe owns an effective 47% of the Kamoa Project, which will decrease to an effective 40% should the additional 15% interest be transferred to the DRC government.

Kamoa is the world’s largest, undeveloped, high-gradecopper deposit. On February 23, 2016, an updated Mineral Resource estimate was issued for the Kamoa Project, with an effective date of May 2014. Kamoa’s Indicated Mineral Resources total 752 million tonnes grading 2.67% copper and containing 44.3 billion pounds of copper at a 1% copper cut-off grade and an approximate minimum true thickness of three metres. In addition to the Indicated Resources, the updated estimate included Inferred Mineral Resources of 185 million tonnes grading 2.08% copper and containing 8.5 billion pounds of copper, also at a 1.0% copper cut-off grade and an approximate minimum true thickness of three metres.

Kamoa 2016 PFS envisages first phase mine production of three million tonnes per year at a grade of 3.86% copper

The Kamoa 2016 PFS, which focuses on the initial phase of development, was filed on March 30, 2016.

Highlights include:

- Mine production of three million tonnes per annum (Mtpa) at an average grade of 3.86% copper over a 24-year mine life, resulting in annual copper production of approximately 100,000 tonnes.

- Initial capital cost, including contingency, is $1.2 billion, approximately $200 million lower than estimated in the Kamoa 2013 PEA.

- Life-of-mine average mine-site cash cost is $0.75/lb. of copper.

- After-tax NPV at an 8% discount rate of $986 million.

- After-tax IRR of 17.2% and a payback period of 4.6 years.

- High-grade copper concentrate with an average grade of 39.2% copper and very low arsenic levels.

- Improvements to the mining method have the potential to reduce average mine site cash cost during the first phase to $0.61/lb. of copper, and improve the after-tax NPV at an 8% discount rate to $1.182 billion, the IRR to 18.9% and the payback period to 4.3 years.

The Kamoa 2016 PFS identified several areas for further evaluation to optimize the project’s economics, including:

- The use of controlled convergence room-and-pillar mining, which has been successfully used by KGHM Polska Miedz S.A. (KGHM) at its copper-mining operations in Poland for the past 20 years. Based on detailed analysis by KGHM Cuprum R&D Centre Ltd., this mining method appears to be well suited to the Kamoa deposit and, if implemented, potentially could provide significant cost savings as there would be no requirement for cemented backfill and ore extraction ratios would increase.

- Increased production up to 4 Mtpa from the proposed initial mining area, with only limited adjustments to the ore-handling and ventilation systems, thereby resulting in a more efficient use of capital.

Ivanhoe and Zijin Mining are working together to define the scope of the feasibility study, taking into account the conclusions and recommendations from the PFS, while critical-path development such as refurbishment of the hydroelectrical facilities at Koni and Mwadingusha continues to progress.

Health and safety at Kamoa

Health and safety remain key priorities for workers and management alike at the Kamoa Project, where an excellent safety record has been achieved. As of April 1, 2016, a total of 4,805,212 hours had been worked without a lost-time injury.

The partnership with Fionet is a collaborative initiative to strengthen local responses to malaria in the DRC under the National Malaria Control Program. To date, 54 health centres in Haut-Katanga and Lualaba provinces are using the intelligent diagnostic device known as the Deki Reader. The device provides step-by-step guidance to health workers, helping to deliver rapid, accurate, diagnostic testing for malaria and transmitting results to a database. Since the program began, 5,393 people have visited the health centres and 4,490 malaria tests have been administered.

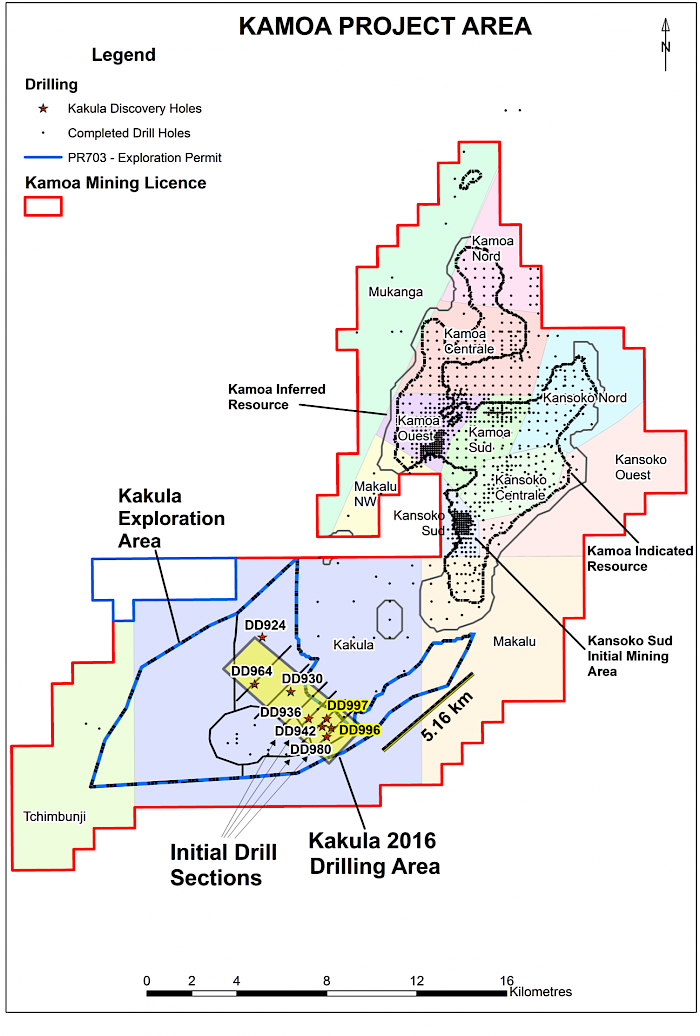

Kamoa exploration team makes major new copper discovery at the Kakula exploration area

Ivanhoe Mines reported on January 25, 2016, that the Kamoa exploration team had made a new, tier-one, high-grade and flat-lying stratiform copper discovery, ideally situated for low-cost mechanized mining, in the Kakula exploration area, approximately five kilometres southwest of the currently defined resources at the Kamoa copper deposit. The Kakula Discovery is located within the 400-square-kilometre Kamoa Mining Licence area and represents a major extension of the Kamoa copper deposit that the company discovered in 2008.

Two exploration drill holes completed in late 2015 in the Kakula exploration area, DD996 and DD997, rank among the highest-grade and highest-grade-thickness intersections drilled to date within the Kamoa copper deposit licence area.

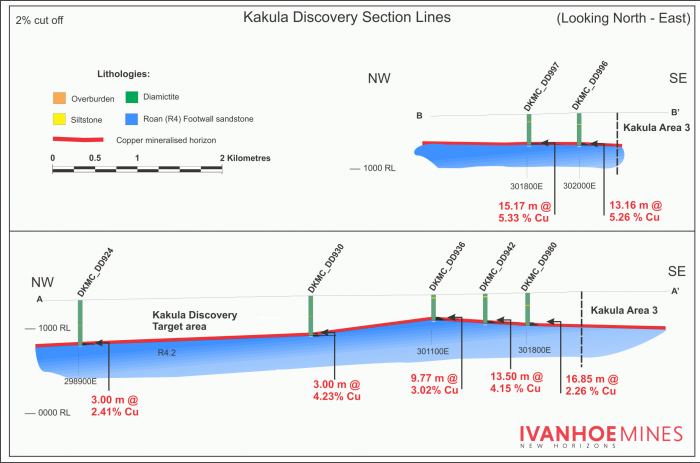

DD996 intersected 24.16 metres (24.13 metres true width) of 3.48% copper, at a 1% copper cut-off. At a higher cut-off of 2% copper, the intersection was 13.16 metres (13.14 metres true width) of 5.26% copper.

DD997 intersected 18.75 metres (18.47 metres true width) of 4.64% copper at a 1% copper cut-off and 15.17 metres (14.94 metres true width) of 5.33% copper at a 2% copper cut-off.

A total of 1,357 metres of exploration drilling was completed in five holes in the area of the Kakula Discovery during Q1 2016. Preparations are underway to increase drilling activity in Q2 2016.

Accelerated and expanded drill program at Kakula Discovery

The Kamoa exploration team plans to accelerate its infill drilling program at the Kakula Discovery area in May 2016. The aim is to complete approximately 25,000 metres of drilling in the area during 2016, for which $5 million has been budgeted. The program will target flat-lying, thick, shallow resources at materially higher grades than the average grades at Kamoa that could potentially improve the economics of the Kamoa pre-feasibility study, once incorporated in the mine plan.

Mineralization at Kakula appears to be consistent in nature with downward vertical zonation from chalcopyrite to bornite to chalcocite in every hole. Mineralization is consistently bottom-loaded, with grades increasing downhole toward the contact between the host Grand Conglomerate and the underlying Mwashia sandstone.

The bottom-loaded nature of Kakula mineralization could support the definition of selective mineralized zones at cut-offs well above the 1% copper cut-off used to define resources at Kamoa. For example, the lower portion of the mineralized intercepts in drill holes DD996 and DD997 intersected 5.59 metres grading 9.16% copper and 7.06 metres grading 8.50% copper, respectively, both at a 3% copper cut-off.

The accelerated drill program initially will focus on a 12-square-kilometre area along the projected trend of mineralization intersected in holes DD996 and DD997, with follow-up infill drilling aimed at defining Indicated Resources in areas where the continuity of higher grades is confirmed. The company is in the process of upgrading access and drill roads in the Kakula Discovery area to support the additional diamond-drill rigs that are being mobilized to site in May. The area of the 2016 drill program is shown in Figure 4.

Figure 4: Kamoa Project area map showing the Kakula exploration area.

Figure 5: Sections across the Kakula Discovery Area.

Updated estimate of Mineral Resources at Kamoa

On February 23, 2016, Ivanhoe Mines released an updated estimate of Mineral Resources as part of its disclosure of the Kamoa 2016 PFS. The Mineral Resources have been defined taking into account the 2014 CIM Definition Standards for Mineral Resources and Mineral Reserves. The Mineral Resource is presented on a 100% project basis, with the attributable effective interest of the Company being 47%.

Table 2: Kamoa Project Indicated and Inferred Mineral Resources (May 2014)

| Category | Tonnage (Mt) |

Area (km 2) |

Copper (%) |

True Thickness (m) |

Contained Copper (kt) |

Contained Copper (billions lbs) |

|---|---|---|---|---|---|---|

| Indicated | 752 | 50.5 | 2.67 | 5.24 | 20,110 | 44.3 |

| Inferred | 185 | 16.8 | 2.08 | 3.87 | 3,840 | 8.5 |

- Dr. Harry Parker and Gordon Seibel, RM of SME, employees of Amec Foster Wheeler, are the Qualified Persons for the Mineral Resource estimate. The effective date of the estimate is May 5, 2014. Mineral Resources are reported inclusive of Mineral Reserves.

- Mineral Resources are reported using a total copper (TCu) cut-off grade of 1% TCu and an approximate minimum true thickness of 3 metres. There are reasonable prospects for eventual economic extraction under assumptions of a copper price of US$3.30/lb; employment of underground mechanized room and pillar and drift-and-fill mining methods; and that copper concentrates will be produced and sold to a smelter. Mining costs are assumed to be $34/t. Concentrator and General and Administrative costs are assumed to be $19/t. Metallurgical recovery will be 77% (supergene) and 85% (hypogene) at the average grade of the resource.

- Reported Mineral Resources contain no allowances for hanging wall or footwall contact boundary loss and dilution. No mining recovery has been applied.

- For Indicated Mineral Resources, 97.4% of the resource model blocks have a true thickness greater than 3 metres (range from 2.3 metres to 15.8 metres), for Inferred Mineral Resources, 94.7% of the resource blocks have a true thickness greater than 3 metres (range from 2.7 metres to 8.4 metres).

- Depth of mineralization below the surface ranges from 10 metres to 1,320 metres for Indicated Mineral Resources and 20 metres to 1,560 metres for Inferred Mineral Resources.

- Approximate drill-hole spacings are 800 metres for Inferred Mineral Resources and 400 metres for Indicated Mineral Resources.

- Rounding as required by reporting guidelines may result in apparent summation differences between tonnes, grade and contained metal content.

First blast at Kamoa declines marks beginning of underground mine development work

Byrnecut Underground Congo SARL (BUCS) is progressing well with the box-cut support work. The work consists of drilling either three- or six-metre holes into the box-cut side walls, supporting a wire mesh cover with either three-metre rebar bolts or six-metre cable anchors and then sealing the mesh with a cover of shotcrete. Bench tops have been sealed by pouring a concrete layer.

Double-boom drill rig drilling three-metre rebar holes on the bottom bench.

Installed mesh and three-metre rebar bolts.

Shotcrete application on the bottom bench.

The first blast at the twin declines at the bottom of the box-cut, marking the beginning of the underground mine development, was successfully conducted on May 12, 2016.

The project team at Kamoa has completed the construction of site offices, a workshop and stores, a vehicle wash bay, a brake test ramp and infrastructure for temporary supply of power and water.

Continued focus on community

Planned community projects for 2016 include the construction of schools and clinics. Kamoa continued with its livelihood sustainability program during Q1 2016. The major areas of activity were maize harvesting and planting, vegetable production, livestock management and bee keeping.

Pest control at the Kamoa farm

Hydroelectric power plant upgrading project

The repairs to turbine number one at the Mwadingusha hydroelectric power plant are progressing and are expected to be completed by the end of June 2016. The repairs are needed to allow the Mwadingusha plant to increase its output of electrical power to the national grid and thereby allow Kamoa to secure 10 megawatts of power from the grid for use during the development of the Kamoa Project. In addition, Kamoa is required to construct a 120kV power line linking the mine to the national grid and procure a substation to be located at the mine to step the voltage down from 120kV to 11kV. Orders have been placed for the power line and the substation.

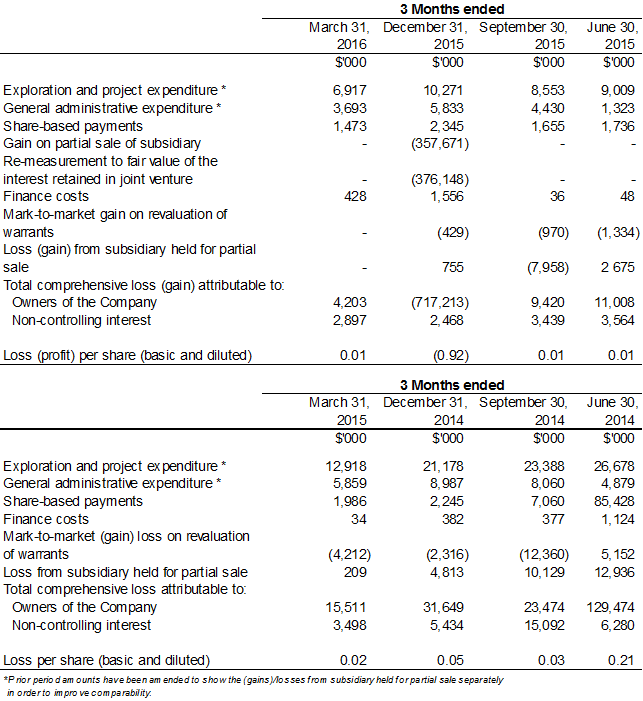

SELECTED QUARTERLY FINANCIAL INFORMATION

The following table summarizes selected financial information for the prior eight quarters. Ivanhoe had no operating revenue in any financial reporting period and did not declare or pay any dividend or distribution in any financial reporting period.

DISCUSSION OF RESULTS OF OPERATIONS

Review of the three months ended March 31, 2016 vs. March 31, 2015

The company’s total comprehensive loss for Q1 2016 of $7.1 million was $11.9 million lower than for the same period in 2015 ($19.0 million). The decrease mainly was due to a $6.0 million decrease in exploration and project expenditure, together with deemed finance income on the purchase price receivable from the partial sale of the Kamoa Project included in other income, which amounted to $4.3 million.

Exploration and project expenditures for the three months ending March 31, 2016, amounted to $6.9 million and were $6.0 million less than for the same period in 2015 ($12.9 million). The $4.1 million retrenchment costs incurred in 2015 relating to the closure of Ivanhoe’s regional exploration company in the DRC were the main reason for the decrease.

With the focus at the Platreef Project on development and the Kamoa Project being accounted for as a joint venture, $6.7 million of the total $6.9 million exploration and project expenditure related to the Kipushi Project. Expenditure at the Kipushi Project decreased by $1.6 million compared to the same period in 2015.

Financial position as at March 31, 2016 vs. December 31, 2015

The company’s total assets decreased by $10.3 million in Q1 2016, from $1,022.6 million as at December 31, 2015, to $1,012.3 million as at March 31, 2016. This mainly was due to the company utilizing its cash resources in its operations.

The remaining purchase-price receivable due to the company as a result of the sale of 49.5% of Kamoa Holding decreased as the company received $51.9 million from Zijin during Q1 2016. The present value of the remaining consideration receivable, net of transaction costs, was $146.9 million as at March 31, 2016. The next of the four remaining installments is due on July 8, 2016.

The company’s investment in the Kamoa Holding joint venture increased by $8.0 million from $412.0 as at December 31, 2015, to $420.0 million as at March 31, 2016, with the current shareholders funding the operations equivalent to their proportionate shareholding interest. At Kamoa, the focus remained on development, together with an exploration program at the Kakula Discovery that will be accelerated in Q2 2016.

Property, plant and equipment increased by $9.7 million, with a total of $10.3 million in Q1 2016 being spent on project development and to acquire other property, plant and equipment, $9.7 million of which was development costs of the Platreef Project.

The company utilized $13.8 million of its cash resources in its operations and earned interest income of $0.7 million on cash balances in the three months ended March 31, 2016; the company’s portion of the Kamoa joint venture cash calls amounted to $7.7 million.

The company generated cash inflow from financing activities during the three months ended March 31, 2016, of $49.7 million. This mainly was a result of proceeds received from Zijin for the partial sale of Kamoa Holding.

The company’s total liabilities decreased to $39.2 million as at March 31, 2016, from $43.8 million as at December 31, 2015. This mainly was due to the decrease in trade and other payables of $4.9 million.

Liquidity and capital resources

The company had $314.0 million in cash and cash equivalents as at March 31, 2016. Certain of the company’s cash and cash equivalents, having an aggregate value of $43.9 million, are subject to contractual restrictions as to their use and are reserved for the Platreef Project.

As at March 31, 2016, the company had consolidated working capital of approximately $438.0 million, compared to $424.6 million at December 31, 2015. The Platreef Project working capital is restricted and amounted to $46.1 million at March 31, 2016, and $53.2 million at December 31, 2015. Excluding the Platreef Project working capital, the resultant working capital was $391.9 million at March 31, 2016, and $371.4 million at December 31, 2015. The company believes it has sufficient resources to cover its short-term cash requirements. However, the company’s access to financing always is uncertain and there can be no assurance that additional funding will be available to the company in the near future.

On December 8, 2015, Zijin completed its investment in Ivanhoe’s Kamoa Copper Project. Zijin, through a subsidiary company, has acquired a 49.5% interest in Kamoa Holding for a total of $412 million in a series of payments. Ivanhoe received an initial $206 million from Zijin on December 8, 2015 and a further $41.2 million on March 23, 2016; the remaining $164.8 million will be received in four equal installments, payable every 3.5 months from the previous installment. Upon closing of the transaction, each shareholder is required to fund Kamoa Holding in an amount equivalent to its proportionate shareholding interest.

The Company’s main objectives for 2016 at the Platreef Project remain the continuation of the phase one feasibility study and Shaft 1 construction. At Kipushi, the principal objective is the continued refurbishment of mining infrastructure, now that the preliminary economic assessment has been successfully completed. At the Kamoa Project, priorities are the continuation of drilling and the construction of the twin declines at Kamoa. The Company expects to spend $32 million on further development at the Platreef Project; $24 million at the Kipushi Project and $18 million on corporate overheads for the remainder of 2016; as well as its proportionate funding of the Kamoa Project, in respect of which expenditures for 2016 are being evaluated with its joint venture partner.

Qualified Person

Disclosures of a scientific or technical nature in this news release have been reviewed and approved by Stephen Torr, who is considered, by virtue of his education, experience and professional association, a Qualified Person under the terms of NI 43-101. Mr. Torr is not considered independent under NI 43-101 as he is the Vice President, Project Geology and Evaluation. Mr. Torr has verified the technical data disclosed in this release.

Ivanhoe has prepared a current independent NI 43-101-compliant technical report for each of the Platreef Project, the Kipushi Project and the Kamoa Project, which are available under the company’s SEDAR profile at www.sedar.com. These technical reports include relevant information regarding the effective date and the assumptions, parameters and methods of the mineral resource estimates on the Platreef Project, the Kipushi Project and the Kamoa Project cited in this release, as well as information regarding data verification, exploration procedures and other matters relevant to the scientific and technical disclosure contained in this release in respect of the Platreef Project, Kipushi Project and Kamoa Project.

Information contacts

Investors

Bill Trenaman +1.604.331.9834

Media

North America: Bob Williamson +1.604.512.4856

South Africa: Jeremy Michaels +27.82.939.4812

Website www.ivanhoemines.com

Forward-looking statements

Certain statements in this release constitute “forward-looking statements” or “forward-looking information” within the meaning of applicable securities laws, including without limitation, the timing and results of: (i) statements regarding the projected depth of Shaft 1 at the Platreef Project and the timing of the commencement of Shaft 2 development, including early works; (ii) statements regarding the operational and technical capacity of Shaft 1; (iii) statements regarding the internal diameter and hoisting capacity of Shaft 2; (iv) statements regarding peak water use of 10 million litres per day at the Platreef Project and development of the Pruissen Pipeline Project; (v) statements regarding the Platreef Project’s electricity requirement; (vi) statements regarding the de-watering program at the Kipushi Project; (vii) statements regarding the completion of the Kipushi Project Environmental, Social and Health Impact Assessment (ESHIA) baseline study; (viii) statements regarding the declines having been designed to intersect the high-grade copper mineralization in the Kansoko Sud area; (ix) statements regarding further drilling at Kakula; (x) statements regarding the timing, size and objectives of drilling and other exploration programs for 2016 and future periods; (xi) statements regarding the completion of installation and repair works at the Mwadingusha power plant; (xii) statements regarding the implementation of Social and Labour Plan at the Platreef Project; (xiii) statement regarding the completion of 25,000 metres of drilling at the Kakula Discovery in 2016; and (xiv) statements regarding expected further expenditure in 2016 of $32 million for the further development of the Platreef Project; and $24 million for the Kipushi Project.

Such statements involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of the company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements or information. Such statements can be identified by the use of words such as “may”, “would”, “could”, “will”, “intend”, “expect”, “believe”, “plan”, “anticipate”, “estimate”, “scheduled”, “forecast”, “predict” and other similar terminology, or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. These statements reflect the company’s current expectations regarding future events, performance and results and speak only as of the date of this release.

As well, the results of the pre-feasibility study of the Kamoa Project, the pre-feasibility study of the Platreef Project and the preliminary economic assessment of the Kipushi Project constitute forward-looking information, and include future estimates of internal rates of return, net present value, future production, estimates of cash cost, proposed mining plans and methods, mine life estimates, cash flow forecasts, metal recoveries, estimates of capital and operating costs and the size and timing of phased development of the projects. Furthermore, with respect to this specific forward-looking information concerning the development of the Kamoa, Platreef and Kipushi Projects, the Company has based its assumptions and analysis on certain factors that are inherently uncertain. Uncertainties include: (i) the adequacy of infrastructure; (ii) geological characteristics; (iii) metallurgical characteristics of the mineralization; (iv) the ability to develop adequate processing capacity; (v) the price of copper, nickel, zinc, platinum, palladium, rhodium and gold; (vi) the availability of equipment and facilities necessary to complete development; (vii) the cost of consumables and mining and processing equipment; (viii) unforeseen technological and engineering problems; (ix) accidents or acts of sabotage or terrorism; (x) currency fluctuations; (xi) changes in regulations; (xii) the compliance by joint venture partners with terms of agreements, (xiii) the availability and productivity of skilled labour; (xiv) the regulation of the mining industry by various governmental agencies; and (xiv) political factors.

This release also contains references to estimates of Mineral Resources and Mineral Reserves. The estimation of Mineral Resources is inherently uncertain and involves subjective judgments about many relevant factors. Estimates of Mineral Reserves provide more certainty but still involve similar subjective judgements. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. The accuracy of any such estimates is a function of the quantity and quality of available data, and of the assumptions made and judgments used in engineering and geological interpretation (including estimated future production from the company’s projects, the anticipated tonnages and grades that will be mined and the estimated level of recovery that will be realized), which may prove to be unreliable and depend, to a certain extent, upon the analysis of drilling results and statistical inferences that ultimately may prove to be inaccurate. Mineral Resource or Mineral Reserve estimates may have to be re-estimated based on: (i) fluctuations in copper, nickel, zinc, platinum group elements (PGE), gold or other mineral prices; (ii) results of drilling; (iii) metallurgical testing and other studies; (iv) proposed mining operations, including dilution; (v) the evaluation of mine plans subsequent to the date of any estimates and/or changes in mine plans; (vi) the possible failure to receive required permits, approvals and licenses; and (vii) changes in law or regulation.

Forward-looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results and will not necessarily be accurate indicators of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from the results discussed in the forward-looking statements, including, but not limited to, the factors discussed below and under “Risk Factors”, as well as unexpected changes in laws, rules or regulations, or their enforcement by applicable authorities; the failure of parties to contracts with the company to perform as agreed; social or labour unrest; changes in commodity prices; and the failure of exploration programs or studies to deliver anticipated results or results that would justify and support continued exploration, studies, development or operations.

Although the forward-looking statements contained in this release are based upon what management of the company believes are reasonable assumptions, the company cannot assure investors that actual results will be consistent with these forward-looking statements. These forward-looking statements are made as of the date of this release and are expressly qualified in their entirety by this cautionary statement. Subject to applicable securities laws, the company does not assume any obligation to update or revise the forward-looking statements contained herein to reflect events or circumstances occurring after the date of this release.

The company’s actual results could differ materially from those anticipated in these forward-looking statements as a result of the factors set forth in the “Risk Factors” section in the company’s MD&A for the three months ended March 31, 2016.