English

English Français

Français 日本語

日本語 中文

中文Preliminary mine redevelopment plan focuses on Kipushi’s Big Zinc Zone and

includes a two-year construction period and life-of-mine average annual

production rate of 530,000 tonnes of zinc concentrate

Kipushi’s Big Zinc Zone has an estimated 10.2 million tonnes

of Measured and Indicated Mineral Resources grading 34.9% zinc

Post-tax NPV of US$533 million and 31% IRR

Successful planned restoration of production would make Kipushi

the world’s highest grade major zinc mine

KIPUSHI, DEMOCRATIC REPUBLIC OF CONGO — Robert Friedland, Executive Chairman of Ivanhoe Mines (TSX: IVN), and Lars-Eric Johansson, Chief Executive Officer, today announced the receipt of an independent, preliminary economic assessment (PEA) for the planned redevelopment of the company’s historic, high-grade, Kipushi zinc-copper mine. The PEA plan covers the redevelopment of Kipushi as an underground mine, producing an average of 530,000 tonnes of zinc concentrate annually over a 10-year mine life at a total cash cost, including copper by-product credits, of approximately US$0.54 per pound of zinc.

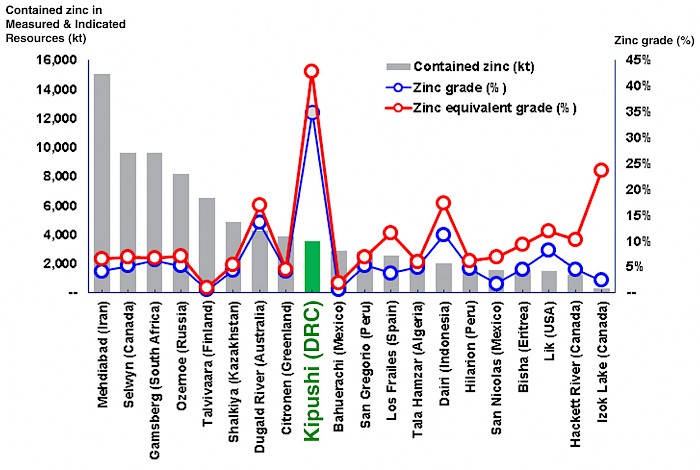

The Kipushi Project is operated by Kipushi Corporation (KICO), a joint venture between Ivanhoe Mines (68%) and Gécamines (32%), the state-owned mining company. The PEA plan focuses on the mining of Kipushi’s Big Zinc Zone, which has an estimated 10.2 million tonnes of Measured and Indicated Mineral Resources grading 34.9% zinc. This grade is more than twice as high as the Measured and Indicated Mineral Resources of the world’s next-highest-grade zinc project, according to Wood Mackenzie, a leading, international industry research and consulting group (see Figure 2, page 6).

The PEA for Kipushi’s redevelopment was prepared by OreWin Pty. Ltd., of Adelaide, Australia, and the MSA Group (Pty.) Ltd., of Johannesburg, South Africa. All monetary figures subsequently stated in this news release are US dollars (US$), unless otherwise stated. The PEA was prepared in compliance with Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects (NI 43-101).

Highlights of the PEA include:

- After-tax net present value (NPV) at an 8% real discount rate is $533 million.

- After-tax real internal rate of return (IRR) is 30.9%.

- After-tax project payback period is 2.2 years.

- Leveraging existing surface and underground infrastructure significantly lowers the redevelopment capital compared to a greenfield development project, as well as the time required to reinstate production.

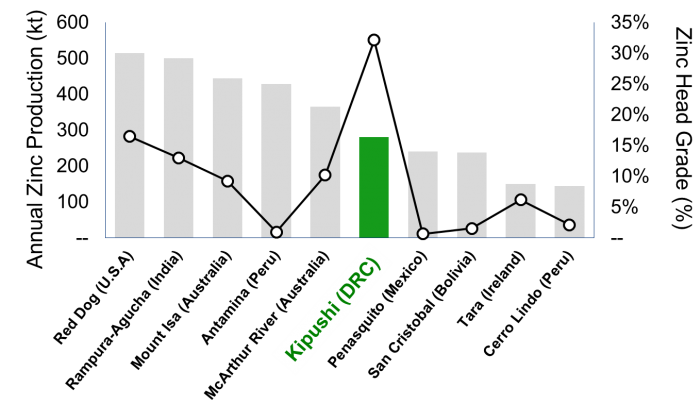

- Life-of-mine average planned zinc concentrate production of 530,000 dry tonnes per annum (tpa), with a concentrate grade of 53% zinc, is expected to rank Kipushi, once in production, among the world’s major zinc mines (see Figure 1, below).

- Life-of-mine average cash cost of US$0.54/lb of zinc is expected to rank Kipushi, once in production, in the bottom quartile of the cash cost curve for zinc producers globally.

“This preliminary mine redevelopment plan supports our view that Kipushi is the best brownfield zinc project in the world,” said Mr. Friedland. “Kipushi’s zinc grade of almost 35% puts the project into a class of its own.”

Independent research by Wood Mackenzie concludes that the Kipushi Project could be expected to rank among the world’s major zinc mines.

Figure 1: World’s major zinc mines(1), showing estimated annual zinc production and zinc head grades.

(1) World’s major zinc mines defined as the world’s 10 largest zinc mines ranked by forecasted production by 2018.

Source: Wood Mackenzie. Note: Independent research by Wood Mackenzie concludes that at the forecast production and head grade, the Kipushi Project, once in production, will rank among the world’s major zinc mines. Wood Mackenzie compared the Kipushi Project’s life-of-mine average annual zinc production and zinc head grade of 281,000 tonnes and 32%, respectively, against production and zinc head grade forecasts for 2018.

“Most of Kipushi’s underground development and infrastructure already is in place and it is expected to be a straightforward, underground mining and milling operation,” said Mr. Friedland.

“The combination of extremely high zinc grades, low capital requirements and low operating costs makes this a compelling development project.

“In April of this year, zinc inventories dropped to the lowest levels since August 2009, providing a great deal of optimism for significantly higher zinc prices in the next few years. As such, we believe that market conditions are ideal as we evaluate the available options to return Kipushi to production,” Mr. Friedland added.

Mr. Johansson said that since beginning operations almost a century ago, Kipushi has written a long and storied history of mining achievement in the Democratic Republic of Congo.

“We are optimistic that the release of this independent, preliminary mine redevelopment plan is a key first step toward redeveloping the mine and beginning the realization of significant benefits for all of the Kipushi Project’s stakeholders, including the Congolese people and our joint-venture partner, Gécamines. As required by our joint venture agreement, we have shared this study with our partner, Gécamines, for its review and approval, and we look forward to working with Gécamines’ experts to further improve the preliminary mine redevelopment plan, where possible,” Mr. Johansson added.

The PEA for the redevelopment of the Kipushi Mine is preliminary in nature and includes an economic analysis that is based, in part, on Inferred Mineral Resources. Inferred Mineral Resources are considered too speculative geologically to have the economic considerations applied to them that would allow them to be categorized as Mineral Reserves, and there is no certainty that the results will be realized. Mineral Resources do not have demonstrated economic viability and are not Mineral Reserves. The Kipushi 2016 PEA recommends that the Kipushi Project is advanced to a pre-feasibility study level in order to increase confidence in the estimates.

Details of Mineral Resource estimates

The Mineral Resource used in the PEA has an effective date of January 23, 2016 and was estimated using The Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Best Practice Guidelines and is reported in accordance with the 2014 CIM Definition Standards, which have been incorporated by reference into NI 43-101. The Mineral Resource is classified into the Measured, Indicated and Inferred categories as shown in Table 1 for the predominantly zinc-rich bodies and in Table 2 for the predominantly copper-rich bodies.

The Mineral Resource estimate was based on the results of 84 holes drilled at Kipushi by Ivanhoe Mines and an additional 107 historical holes drilled by Gécamines. Ivanhoe completed its drilling program for the Mineral Resource estimate in October 2015. Mineral Resource estimates were completed below the -1,150-metre-level on the Big Zinc Zone, Southern Zinc Zone, Fault Zone and Série Récurrente Zone. The Mineral Resources were categorized either as zinc-rich resources or copper-rich resources, depending on the most abundant metal. The Big Zinc and Southern Zinc zones have been tabulated using zinc cut-offs and are shown in Table 1; the Fault Zone, the Fault Zone Splay and Série Récurrente Zone have been tabulated using copper cut-offs and are shown in Table 2. For the zinc-rich zones, the Mineral Resource is reported at a base-case cut-off grade of 7.0% zinc and the copper-rich zones at a base-case cut-off grade of 1.5% copper.

Table 1: Kipushi zinc-rich Mineral Resource at 7% zinc cut-off grade, 23 January 2016

| Zone | Category | Tonnes (millions) |

Zn % |

Cu % |

Pb % |

Ag g/t |

Co ppm |

Ge g/t |

|||||

| Big Zinc | Measured | 3.59 | 38.39 | 0.67 | 0.36 | 18 | 17 | 54 | |||||

| Indicated | 6.60 | 32.99 | 0.63 | 1.29 | 20 | 14 | 50 | ||||||

| Inferred | 0.98 | 36.96 | 0.79 | 0.14 | 7 | 16 | 62 | ||||||

| Southern Zinc | Indicated | 0.00 | – | – | – | – | – | – | |||||

| Inferred | 0.89 | 18.70 | 1.61 | 1.70 | 13 | 15 | 43 | ||||||

| Total | Measured | 3.59 | 38.39 | 0.67 | 0.36 | 18 | 17 | 54 | |||||

| Indicated | 6.60 | 32.99 | 0.63 | 1.29 | 20 | 14 | 50 | ||||||

| Measured & Indicated | 10.18 | 34.89 | 0.65 | 0.96 | 19 | 15 | 51 | ||||||

| Inferred | 1.87 | 28.24 | 1.18 | 0.88 | 10 | 15 | 53 | ||||||

| Contained metal quantities | |||||||||||||

| Zone | Category | Tonnes (millions) |

Zn (million lbs) |

Cu (million lbs) |

Pb (million lbs) |

Ag (million oz) |

Co (million lbs) |

Ge (millionoz) |

|||||

| Big Zinc | Measured | 3.59 | 3,035.8 | 53.1 | 28.7 | 2.08 | 0.13 | 6.18 | |||||

| Indicated | 6.60 | 4,797.4 | 91.9 | 187.7 | 4.15 | 0.20 | 10.54 | ||||||

| Inferred | 0.98 | 797.2 | 17.1 | 3.0 | 0.23 | 0.03 | 1.96 | ||||||

| Southern Zinc | Indicated | 0.00 | 0.0 | 0.0 | 0.0 | 0.00 | 0.00 | 0.00 | |||||

| Inferred | 0.89 | 368.6 | 31.8 | 33.5 | 0.38 | 0.03 | 1.23 | ||||||

| Total | Measured | 3.59 | 3,035.8 | 53.1 | 28.7 | 2.08 | 0.13 | 6.18 | |||||

| Indicated | 6.60 | 4,797.4 | 91.9 | 187.7 | 4.15 | 0.20 | 10.54 | ||||||

| Measured & Indicated | 10.18 | 7,833.3 | 144.9 | 216.4 | 6.22 | 0.33 | 16.71 | ||||||

| Inferred | 1.87 | 1,168.7 | 49.6 | 36.8 | 0.61 | 0.06 | 3.21 | ||||||

Notes:

- All tabulated data has been rounded and as a result minor computational errors may occur.

- Mineral Resources that are not Mineral Reserves have no demonstrated economic viability.

- The Mineral Resource is reported as the total in-situ Mineral Resource.

- Metal quantities are reported in multiples of Troy Ounces or Avoirdupois Pounds.

- The cut-off grade calculation was based on the following assumptions: zinc price of $1.02 /lb, mining cost of $50 /tonne, processing cost of $10 /tonne, G&A and holding cost of $10 /tonne, transport of 55% Zn concentrate at $375 /tonne, 90% zinc recovery and 85% payable zinc.

Table 2: Kipushi Copper-Rich Mineral Resource at 1.5% Copper cut-off grade, 23 January 2016

| Zone | Category | Tonnes (millions) |

Cu % |

Zn % |

Pb % |

Ag g/t |

Co ppm |

Ge g/t |

||||||

| Fault Zone | Measured | 0.14 | 2.78 | 1.25 | 0.05 | 19 | 107 | 20 | ||||||

| Indicated | 1.01 | 4.17 | 2.64 | 0.09 | 23 | 216 | 20 | |||||||

| Inferred | 0.94 | 2.94 | 5.81 | 0.18 | 22 | 112 | 26 | |||||||

| Série Récurrenté | Indicated | 0.48 | 4.01 | 3.82 | 0.02 | 21 | 56 | 6 | ||||||

| Inferred | 0.34 | 2.57 | 1.02 | 0.06 | 8 | 29 | 1 | |||||||

| Fault Zone Splay | Inferred | 0.35 | 4.99 | 15.81 | 0.005 | 20 | 127 | 81 | ||||||

| Total | Measured | 0.14 | 2.78 | 1.25 | 0.05 | 19 | 107 | 20 | ||||||

| Indicated | 1.49 | 4.12 | 3.02 | 0.07 | 22 | 165 | 15 | |||||||

| Measured & Indicated | 1.63 | 4.01 | 2.87 | 0.06 | 22 | 160 | 16 | |||||||

| Inferred | 1.64 | 3.30 | 6.97 | 0.12 | 19 | 98 | 33 | |||||||

| Contained metal quantities | ||||||||||||||

| Zone | Category | Tonnes (millions) |

Cu lbs (millions) |

Zn lbs (millions) |

Pb lbs (millions) |

Ag oz (millions) |

Co lbs (millions) |

Ge oz (millions) |

||||||

| Fault Zone | Measured | 0.14 | 8.5 | 3.8 | 0.2 | 0.09 | 0.03 | 0.09 | ||||||

| Indicated | 1.01 | 93.2 | 59.1 | 1.9 | 0.75 | 0.48 | 0.64 | |||||||

| Inferred | 0.94 | 61.1 | 120.9 | 3.8 | 0.68 | 0.23 | 0.79 | |||||||

| Série Récurrenté | Indicated | 0.48 | 42.4 | 40.5 | 0.2 | 0.32 | 0.06 | 0.09 | ||||||

| Inferred | 0.34 | 19.4 | 7.7 | 0.4 | 0.09 | 0.02 | 0.01 | |||||||

| Fault Zone Splay | Inferred | 0.35 | 38.9 | 123.3 | 0.0 | 0.23 | 0.10 | 0.92 | ||||||

| Total | Measured | 0.14 | 8.5 | 3.8 | 0.2 | 0.09 | 0.03 | 0.09 | ||||||

| Indicated | 1.49 | 135.7 | 99.6 | 2.1 | 1.08 | 0.54 | 0.73 | |||||||

| Measured & Indicated | 1.63 | 144.1 | 103.4 | 2.3 | 1.16 | 0.58 | 0.82 | |||||||

| Inferred | 1.64 | 119.4 | 251.8 | 4.3 | 1.00 | 0.35 | 1.73 | |||||||

Notes:

- All tabulated data has been rounded and as a result minor computational errors may occur.

- Mineral Resources that are not Mineral Reserves have no demonstrated economic viability.

- The Mineral Resource is reported as the total in-situ Mineral Resource.

- Metal quantities are reported in multiples of Troy Ounces or Avoirdupois Pounds.

- The cut-off grade calculation was based on the following assumptions: copper price of $2.97 /lb, mining cost of $50/tonne, processing cost of $10/tonne, G&A and holding cost of $10/tonne, 90% copper recovery and 96% payable copper.

Exploration drilling conducted by Ivanhoe Mines in 2015 sucessfully confirmed that both the Big Zinc Zone and Fault Zone remain open at depth and to the south. Additional high-grade copper-zinc-germanium mineralization also was discovered in the Fault Zone and in the Fault Zone Splay in the immediate footwall of the Fault Zone.

Figure 2: Top 20 zinc projects by contained zinc

Source: Wood Mackenzie. Note: All tonnes and metal grades of individual metals used in the equivalency calculation of the above mentioned projects (except for Kipushi) are based on public disclosure and have been compiled by Wood Mackenzie. All metal grades have been converted by Wood Mackenzie to a zinc equivalent grade at price assumptions of $1.01/lb zinc, $2.86/lb copper, $0.91/lb lead, $12.37/lb cobalt, $1,201/oz gold, $17/oz silver and $2,000/kg germanium.

Existing underground infrastructure and mining

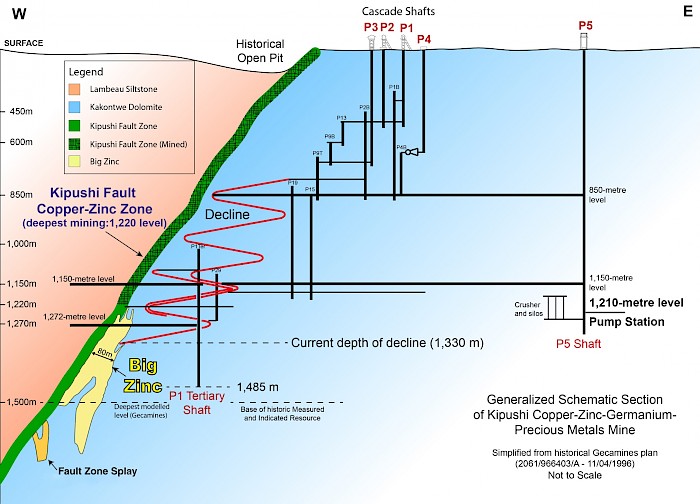

Historical mining at Kipushi was carried out from surface to approximately 1,220 metres below surface (mL) and occurred in three contiguous zones: The North and South zones of the Fault Zone, and the Série Récurrente Zone in the footwall of the fault that is approximately east-west striking and steeply north dipping.

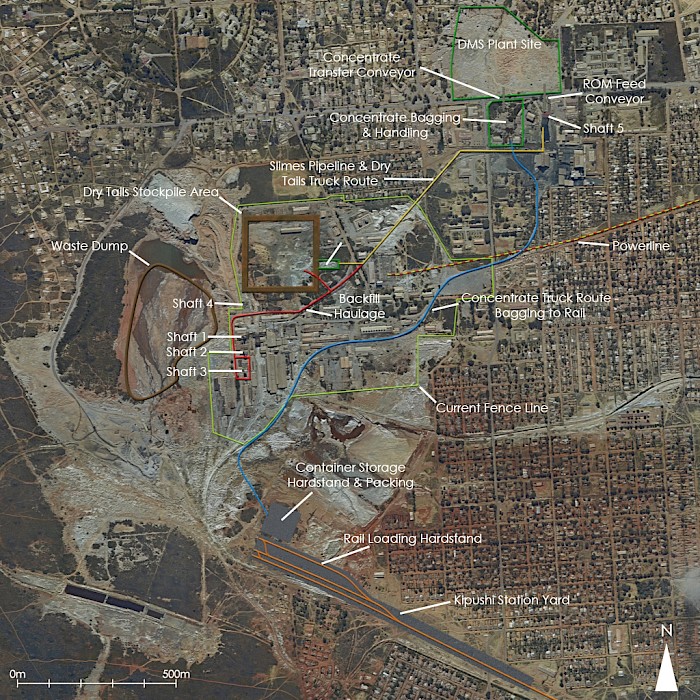

KICO has a significant amount of underground infrastructure at the Kipushi Project, including a series of vertical mine shafts, with associated head frames, to various depths, as well as underground mine excavations. A schematic layout of the existing development is shown in Figure 3.

The newest shaft, # 5 (labeled as P5 in Figure 3 below), is eight metres in diameter and 1,240 metres deep. It is expected to be recommissioned as the main production shaft. It has a maximum hoisting capacity of 1.8 million tonnes a year (Mtpa) and provides the primary access to the lower levels of the mine, including the Big Zinc Zone, through the 1,150mL haulage level. Shaft 5 is located approximately 1.5 kilometres from the main mining area. A series of crosscuts and ventilation infrastructure still are in working condition. The underground infrastructure also includes a series of pumps to manage the influx of water into the mine.

Figure 3: Schematic section of Kipushi Mine

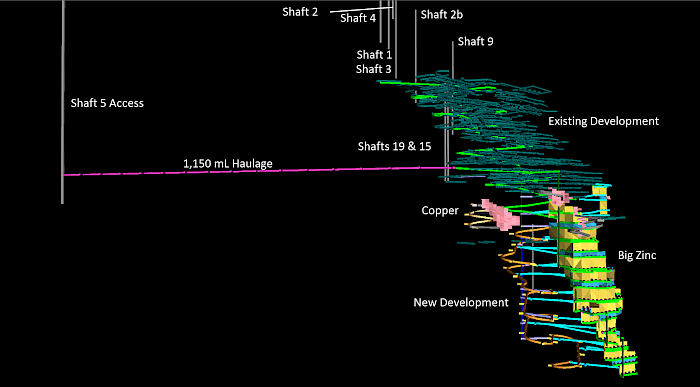

The planned mining method is a combination of Sublevel Open Stoping (SLOS), Pillar Retreat and Cut and Fill methods at a steady-state mining rate of 1.1 Mtpa. The existing and planned development is shown in Figure 4.

The primary mining method for the Big Zinc Zone in the PEA is expected to be SLOS, with cemented rock backfill. The crown pillars are expected to be mined once adjacent stopes are backfilled using a Pillar Retreat mining method. The Big Zinc Zone is expected to be accessed via the existing decline and without significant new development. The main levels are planned to be at 60-metre vertical intervals, with sublevels at 30-metre intervals.

The Cut and Fill mining method has been identified to be used to extract the copper zone outside the Big Zinc Zone. In this method, mining occurs in horizontal slices, with the blasted copper material removed from the stopes, then crushed underground and sold at the mine gate.

Figure 4: Planned and existing development at Kipushi

Zinc processing by dense media separation

The planned process plant in the PEA is a dense media separation (DMS) plant, which is expected to include crushing, screening, heavy-liquid separation (HLS) and spirals to produce a high-grade zinc concentrate. DMS is a simple density concentration technique that preliminary testwork has shown yields positive results for the Kipushi material, which has a sufficient density differential between the gangue (predominantly dolomite) and mineralization (sphalerite). DMS washability profiles were evaluated in the laboratory at three feed-crush sizes using a combination of HLS and shaking tables.

Preliminary test work results on three crush sizes indicated that the –20-mm crush size resulted in the highest recovery and concentrate grade. This crush size achieved an overall recovery of 95.4% at a concentrate grade of 55.5% zinc.

Infrastructure

The Kipushi Project includes surface mining and processing infrastructure, concentrator, offices, workshops and a connection to the national power grid. Electricity is supplied by the Democratic of the Congo’s (DRC) state power company, Société Nationale d’Electricité (SNEL), from two transmission lines from Lubumbashi. Pylons are in place for a third line.

The surface infrastructure is owned by Gécamines. KICO has entered into an agreement to use the surface rights on the Kipushi Project to the extent required for its operations.

An abundant supply of process water from the underground dewatering operations is expected to provide adequate water for processing and mining operations.

The overall proposed site layout is shown in Figure 5.

Figure 5: Proposed site layout

The Kipushi Station and connecting rail line from Kipushi to Manama, and through to the Zambian border at Ndola, are owned and operated by La Société Nationale des Chemins de Fer du Congo (SNCC).

The proposed export route is to utilize the SNCC network from Kipushi to Ndola, connecting to the North-South Rail Corridor from Ndola to Durban. The Kipushi to Manama branch line will require a significant refurbishment over 30 kilometres (the required capital is expected to be repaid through the estimated transport cost of $250 per tonne). The North-South Rail Corridor from Sakania to Durban via Zimbabwe is fully operational and has a capacity of 5 Mtpa. Ivanhoe Mines is working with Grindrod Limited, of South Africa, a leading and experienced freight services, shipping and financial services logistics operator in Southern Africa, to advance discussions with SNCC regarding the concession from Kipushi to Manama.

Proposed mine production

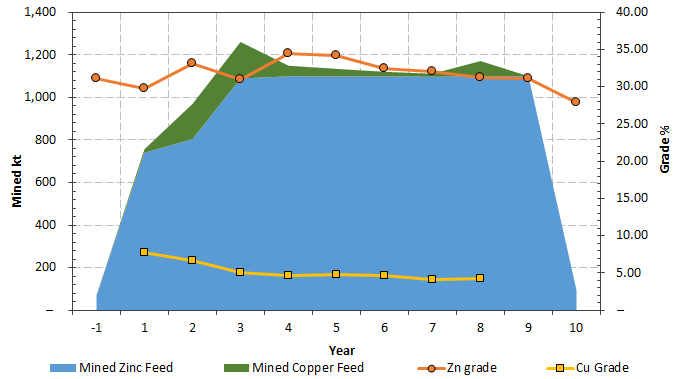

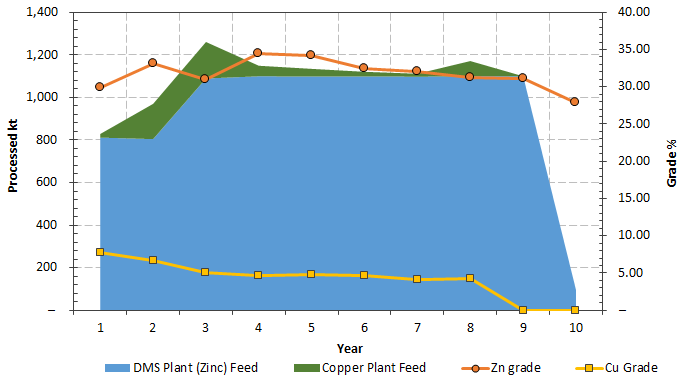

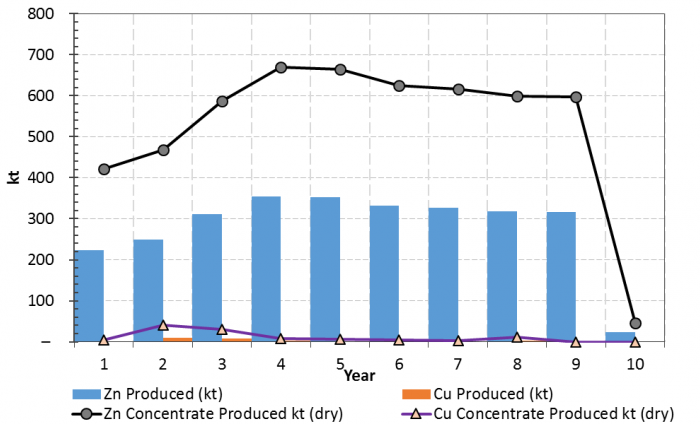

Future proposed mine production has been scheduled to maximize the mine output and meet the DMS plant capacity. The mining production forecasts are shown in Table 3. Mine, process and concentrate production are shown in figures 6 to 8.

Table 3: Mining production statistics

| Description | Unit | Total LOM | 5-Year Average | LOM Average |

| Zinc feed – tonnes processed | ||||

| Quantity Zinc Tonnes Treated | kt | 9,394 | 981 | 939 |

| Zinc Feed grade | % | 32.15 | 32.65 | 32.15 |

| Zinc Recovery | % | 92.94 | 93.14 | 92.94 |

| Zinc Concentrate Produced | kt (dry) | 5,296 | 562 | 530 |

| Zinc Concentrate grade | % | 53.00 | 53.00 | 53.00 |

| Copper feed – tonnes processed | ||||

| Quantity Copper Tonnes Treated | kt | 547 | 88 | 55 |

| Copper Feed grade | % | 5.41 | 5.68 | 5.41 |

| Copper Recovery | % | 90.00 | 90.00 | 90.00 |

| Copper Concentrate Produced | kt (dry) | 106 | 18 | 11 |

| Copper Concentrate grade | % | 25.00 | 25.00 | 25.00 |

| Metal produced | ||||

| Zinc | kt | 2,807 | 298 | 281 |

| Copper | kt | 27 | 4 | 3 |

Figure 6: Zinc and copper – tonnes mined

Figure 7: Zinc and copper – tonnes processed

Figure 8: Concentrate and metal production

Economic analysis

The estimates of cash flows have been prepared on a real basis as at January 1, 2016, and a mid-year discounting is used to calculate the NPV.

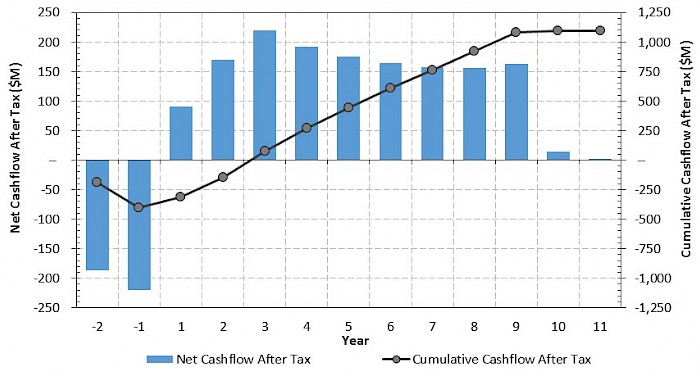

The projected financial results for undiscounted and discounted cash flows, at a range of discount rates, IRR and payback are shown in Table 4. The key economic assumptions for the discounted cash flow analyses are shown in Table 5. The results of NPV sensitivity analysis to a range of zinc prices and discount rates is shown in Table 6. A chart of the cumulative cash flow is shown in Figure 9.

Table 4: Financial results

| Description | Discount Rate | Before Taxation | After Taxation |

| Net Present Value ($M) | Undiscounted | 1,473 | 1,076 |

| 5.0% | 973 | 696 | |

| 8.0% | 759 | 533 | |

| 10.0% | 642 | 444 | |

| 12.0% | 542 | 368 | |

| Internal Rate of Return | – | 36.4% | 30.9% |

| Project Payback Period (Years) | – | 2.1 | 2.2 |

Table 5: Metal prices and terms

| Parameter | Unit | Financial Analysis Assumption |

| Zinc Price | $/t | 2,227 |

| Copper Price | $/t | 6,614 |

| Zinc Treatment Charge | $/t concentrate | 200.00 |

| Copper Treatment Charge | $/t concentrate | 90.00 |

| Copper Refining Charge | $/t Cu | 198.42 |

Table 6: After-tax NPV sensitivity to zinc prices and discount rates

| Discount Rate | Zinc ($/t) | ||||||

| 1,500 | 1,750 | 2,000 | 2,227 | 2,500 | 2,750 | 3,000 | |

| Undiscounted | -157 | 325 | 719 | 1,076 | 1,507 | 1,901 | 2,295 |

| 5% | -210 | 146 | 436 | 696 | 1,008 | 1,293 | 1,577 |

| 8% | -230 | 69 | 315 | 533 | 794 | 1,032 | 1,269 |

| 10% | -240 | 28 | 249 | 444 | 677 | 889 | 1,101 |

| 12% | -248 | -7 | 193 | 368 | 577 | 767 | 957 |

Figure 9: Cumulative cash flow

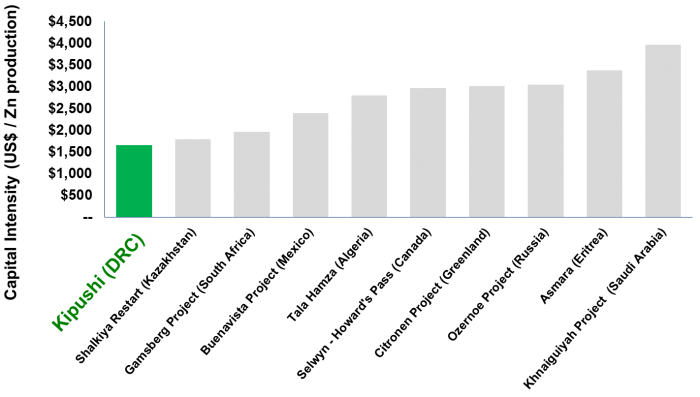

The total capital cost estimates for Kipushi are shown in Table 7. Kipushi’s estimated low capital intensity relative to comparable “probable” and “base case” zinc projects identified by Wood Mackenzie is highlighted in Figure 10, page 16.

Table 7: Estimated capital costs

| Description | Pre-Production ($M) |

Sustaining ($M) |

Total ($M) |

| Mining: | |||

| Rehabilitation | 111 | – | 111 |

| Underground | 52 | 84 | 136 |

| Capitalized Mining Operating Costs | 37 | – | 37 |

| Subtotal | 200 | 84 | 284 |

| Process & Infrastructure: | |||

| Process & Infrastructure | 32 | 6 | 38 |

| Subtotal | 32 | 6 | 38 |

| Closure: | |||

| Closure | – | 20 | 20 |

| Subtotal | – | 20 | 20 |

| Indirects: | |||

| EPCM | 29 | 2 | 32 |

| Capitalized G&A & Other Costs | 60 | – | 60 |

| Subtotal | 89 | 2 | 92 |

| Others: | |||

| Owners Cost | 29 | 2 | 32 |

| Capital Cost Before Contingency | 350 | 115 | 465 |

| Contingency | 58 | 4 | 63 |

| Capital Cost After Contingency | 409 | 119 | 528 |

Figure 10: Capital intensity for zinc projects

Figure based on data from Wood Mackenzie, April 2016. Note: All comparable “probable” and “base case” projects as identified by Wood Mackenzie. Source: Wood Mackenzie (based on public disclosure and information gathered in the process of routine research. The Kipushi 2016 PEA has not been reviewed by Wood Mackenzie).

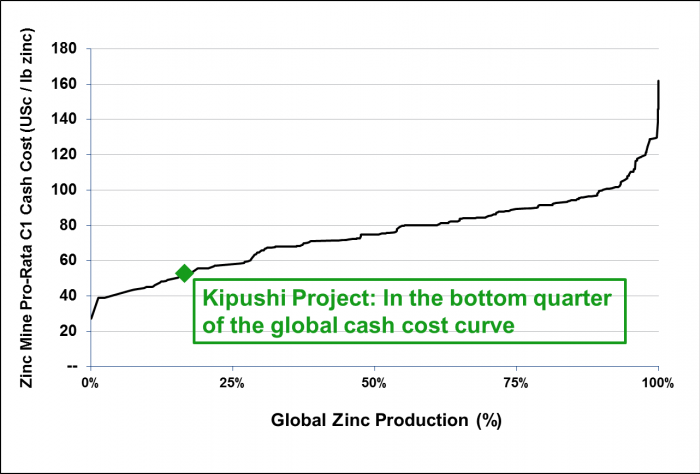

Kipushi’s estimated revenues and operating costs are presented in Table 8, along with the projected net sales revenue value attributable to each key period of operation. Kipushi’s estimated cash costs are presented in Table 9. Based on data from Wood Mackenzie, life-of-mine average cash cost of US$0.54/lb of zinc is expected to rank Kipushi, once in production, in the bottom quartile of the 2018 cash cost curve for zinc producers globally (see Figure 11, page 18).

Table 8: Estimated operating costs and revenues

| Description | Total ($M) |

5-Year Average | LOM Average |

| ($/t Milled) | |||

| Revenue: | |||

| Gross Sales Revenue | 5,481 | 555 | 551 |

| Less Realization Costs: | |||

| Transport Costs | 1,466 | 147 | 147 |

| Treatment & Refining Charges | 1,074 | 108 | 108 |

| Royalties | 198 | 20 | 20 |

| Total Realization Costs | 2,737 | 275 | 275 |

| Net Sales Revenue | 2,744 | 279 | 276 |

| Less Site Operating Costs: | |||

| Mining | 536 | 58 | 54 |

| Processing Zn and Cu (tolling) | 87 | 10 | 9 |

| General & Administration | 120 | 11 | 12 |

| Total | 743 | 79 | 75 |

| Operating Margin ($M) | 2,001 | 201 | 201 |

| Operating Margin (%) | 37 | 36 | 37 |

Table 9: Estimated cash costs

| Description | 5-Year Average | LOM Average |

| ($/lb Payable Zn) | ||

| Mine Site Cash Cost | 0.13 | 0.12 |

| Realization | 0.45 | 0.44 |

| Total Cash Costs Before Credits | 0.58 | 0.56 |

| Copper Credits | (0.04) | (0.03) |

| Total Cash Costs After Credits | 0.53 | 0.54 |

Figure 11: 2018 expected C1 cash costs

Figure based on data from Wood Mackenzie, April 2016. Note: Represents C1 pro-rata cash costs which reflect the direct cash costs of producing paid metal incorporating mining, processing and offsite realization costs, having made appropriate allowance for the co-product revenue streams. Source: Wood Mackenzie (based on public disclosure and information gathered in the process of routine research. The Kipushi 2016 PEA has not been reviewed by Wood Mackenzie).

Figure 12: Y-junction on 1,200-metre level. Silos to the right and cage to the left

Figure 13: Off-loading new wire rope for the Shaft 5 hoist

Qualified Persons, Quality Control and Assurance

The Qualified Persons for the Kipushi 2016 PEA are:

- Bernard Peters, B. Eng. (Mining), FAusIMM (201743), employed by OreWin as Technical Director – Mining.

- Michael Robertson, BSc Eng. (Mining Geology), MSc (Structural Geology), Pr.Sci.Nat SACNASP, MGSSA, MSEG, MSAIMM, employed by MSA as a Principal Consulting Geologist.

- Jeremy Witley, BSc Hons (Mining Geology), MSc (Eng), Pr.Sci.Nat SACNASP, FGSSA, employed by MSA as a Principal Resource Consultant.

All three individuals are independent of Ivanhoe Mines and all have the appropriate relevant qualifications and experience to be considered an independent Qualified Person under the terms of NI 43-101. Messrs. Peters, Robertson and Witley have approved the disclosure of technical information on the Kipushi 2016 PEA contained in this news release and have verified the technical data related thereto.

Other scientific and technical information in this news release has been reviewed and approved by Stephen Torr, P.Geo., Ivanhoe Mines’ Vice President, Project Geology and Evaluation, a Qualified Person under the terms of NI 43-101. Mr. Torr is not independent of Ivanhoe Mines. Mr. Torr has verified the technical data disclosed in this news release not related to the current Mineral Resource estimate disclosed herein.

Ivanhoe Mines maintains a comprehensive chain of custody and QA-QC program on assays from its Kipushi Project. Half-sawn core was processed either at its preparation laboratory in Kamoa, DRC, or its exploration preparation laboratory in Kolwezi, DRC. Prepared samples then were shipped to Bureau Veritas Minerals (BVM) Laboratories in Australia for external assay. Industry-standard certified reference materials and blanks were inserted into the sample stream prior to dispatch to BVM. Ivanhoe Mines’ QA-QC program has been set up in consultation with MSA Group (Pty.) Ltd., of Johannesburg.

Ivanhoe Mines will be filing a NI 43-101 Technical Report for the Kipushi 2016 PEA disclosed herein, within 45 days of this news release.

About Ivanhoe Mines

In addition to the Kipushi Project, Ivanhoe Mines is developing two other principal projects:

- The Kamoa copper discovery in a previously unknown extension of the Central African Copperbelt in the Democratic Republic of Congo’s southern Lualaba province. On December 8, 2015, Ivanhoe and China’s Zijin Mining Group completed a landmark agreement to co-develop the world-scale Kamoa discovery.

- A multi-phased mine development on its 64%-owned Platreef discovery of platinum, palladium, nickel, copper, gold and rhodium in South Africa’s Bushveld Complex. The South African beneficiaries of a broad-based, black economic empowerment structure have a 26% stake in the Platreef Project and the remaining 10% is owned by a Japanese consortium of ITOCHU Corporation; Japan Oil, Gas and Metals National Corporation; ITC Platinum Development Ltd., an ITOCHU affiliate; and JGC Corporation.

Information contacts

Investors

Bill Trenaman +1.604.331.9834

Media

North America: Bob Williamson +1.604.512.4856

South Africa: Jeremy Michaels +27.82.939.4812

Website www.ivanhoemines.com

FORWARD-LOOKING STATEMENTS

Statements in this news release that are forward-looking statements are subject to various risks and uncertainties concerning the specific factors disclosed here and elsewhere in the company’s periodic filings with Canadian securities regulators. When used in this document, the words such as “could,” “plan,” “estimate,” “expect,” “intend,” “may,” “potential,” “should” and similar expressions, are forward-looking statements. Information provided in this document is necessarily summarized and may not contain all available material information.

All of the results of the Kipushi 2016 PEA represent forward-looking information and statements. Statements in this news release that constitute forward-looking statements or information include, but are not limited to: statements about the Kipushi Project having an after-tax NPV of $533 million and an IRR of 30.9%; statements regarding pre-production capital estimated at $409 million; statements about future mine production including that mine production is expected to be at a steady-state mining rate of 1.1 Mtpa, that life-of-mine average planned zinc concentrate production is 530,000 tpa with a concentrate grade of 53%, and that the planned life-of-mine average annual zinc production is 281,000 tonnes and zinc head grade is 32%; statements regarding the proposed rail export route for zinc concentrate to the port of Durban, South Africa; statements about life of mine production of 2,807 kt zinc and 27 kt copper; statements about total cash cost, including by-product credits, of $0.54 per pound of zinc; and statements regarding expected methods of mining and processing.

The forward-looking information and statements also includes metal price assumptions, cash flow forecasts, projected capital and operating costs, metal recoveries, mine life and production rates, and other assumptions used in the Kipushi 2016 PEA. Readers are cautioned that actual results may vary from those presented. The factors and assumptions used to develop the forward-looking information, and the risks that could cause the actual results to differ materially are presented in the body of the Technical Report that will be filed on SEDAR at www.sedar.com and Ivanhoe Mines’ website at www.ivanhoemines.com within 45 days of this news release.

All such forward-looking information and statements are based on certain assumptions and analyses made by Ivanhoe Mines’ management in light of their experience and perception of historical trends, current conditions and expected future developments, as well as other factors management believe are appropriate in the circumstances. These statements, however, are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information or statements including, but not limited to, unexpected changes in laws, rules or regulations, or their enforcement by applicable authorities; the failure of parties to contracts to perform as agreed; social or labour unrest; changes in commodity prices; unexpected failure or inadequacy of infrastructure, or delays in the refurbishment or development of infrastructure, and the failure of exploration programs or other studies to deliver anticipated results or results that would justify and support continued studies, development or operations. Other important factors that could cause actual results to differ from these forward-looking statements also include those described under the heading “Risk Factors” in the company’s most recently filed MD&A as well as in the most recent Annual Information Form filed by Ivanhoe Mines. Readers are cautioned not to place undue reliance on forward-looking information or statements.

This press release also contains references to estimates of Mineral Resources. The estimation of Mineral Resources is inherently uncertain and involves subjective judgments about many relevant factors. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. The accuracy of any such estimates is a function of the quantity and quality of available data, and of the assumptions made and judgments used in engineering and geological interpretation, which may prove to be unreliable and depend, to a certain extent, upon the analysis of drilling results and statistical inferences that may ultimately prove to be inaccurate. Mineral Resource estimates may have to be re-estimated based on, among other things: (i) fluctuations in zinc, copper, or other mineral prices; (ii) results of drilling; (iii) results of metallurgical testing and other studies; (iv) changes to proposed mining operations, including dilution; (v) the evaluation of mine plans subsequent to the date of any estimates; and (vi) the possible failure to receive required permits, approvals and licences.

Although the forward-looking statements contained in this release are based upon what management of the company believes are reasonable assumptions, the company cannot assure investors that actual results will be consistent with these forward-looking statements. These forward-looking statements are made as of the date of this release and are expressly qualified in their entirety by this cautionary statement. Subject to applicable securities laws, the company does not assume any obligation to update or revise the forward-looking statements contained herein to reflect events or circumstances occurring after the date of this release.